Deck Review with XOMA

Surveying great inventors and businesses

Axial partners with great founders and inventors. We invest in early-stage life sciences companies such as Appia Bio, Seranova Bio, Delix Therapeutics, Simcha Therapeutics, among others often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you - email us at info@axialvc.com

XOMA was founded in 1981 centered around an antibody phage display library and with foundational optimization and expression technologies. XOMA was a peer to Genentech - the latter became an iconic drug company while the former spent over $1B over its lifetime without an approved product (XOMA did own a single-digit royalty on Raptiva, which was pulled from the market due to safety concerns). I remember meeting the management team around 2015 and was amazed about the size and depth of their antibody library.

In 2017, after ~40 years of failing to commercialize their own medicines, XOMA pivoted from a traditional biotechnology company to a royalty aggregator. XOMA buys potential milestones and royalty payments on clinical drug candidates. The business of monetizing later stage clinical and approved products is well served by Ligand and Royalty Pharma, respectively. XOMA made the smart move to build a similar business model but focused on earlier-stage clinical assets.

The first slide of their latest corporate presentation states their business model: royalty aggregation.

The next slide gives an overview of XOMA’s business: a portfolio of over 65 preclinical, early-stage drug candidates.

XOMA’s business model relies on providing another capital raising pathway for an early-stage biotechnology company.

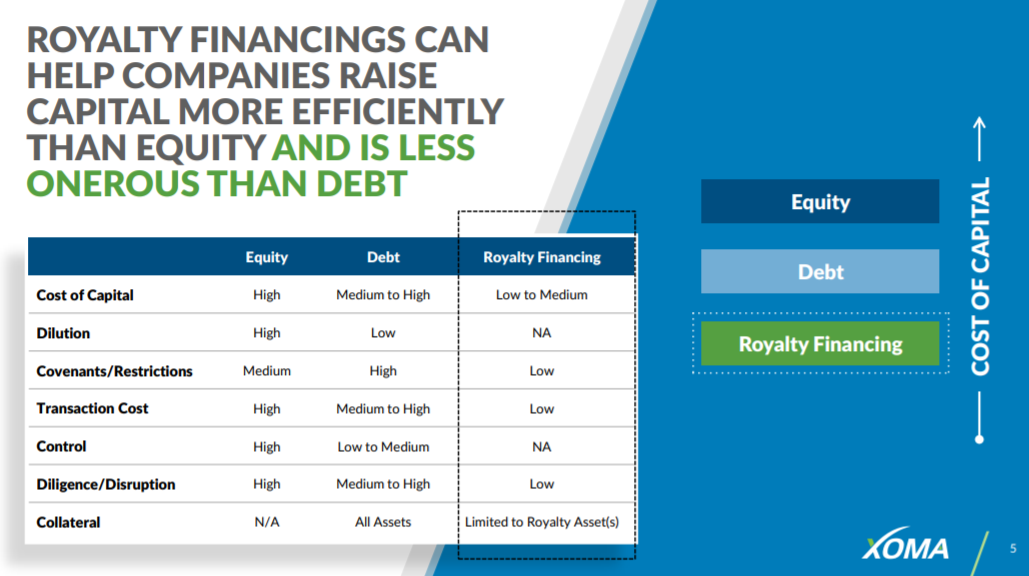

This slide gives an overview on royalty financing. XOMA wants to argue that raising capital by selling drug royalties has a lower cost of capital than equity or debt; they have every incentive to try to say this. Royalty financing can be very expensive if a drug becomes a blockbuster if it wasn’t expected to be one.

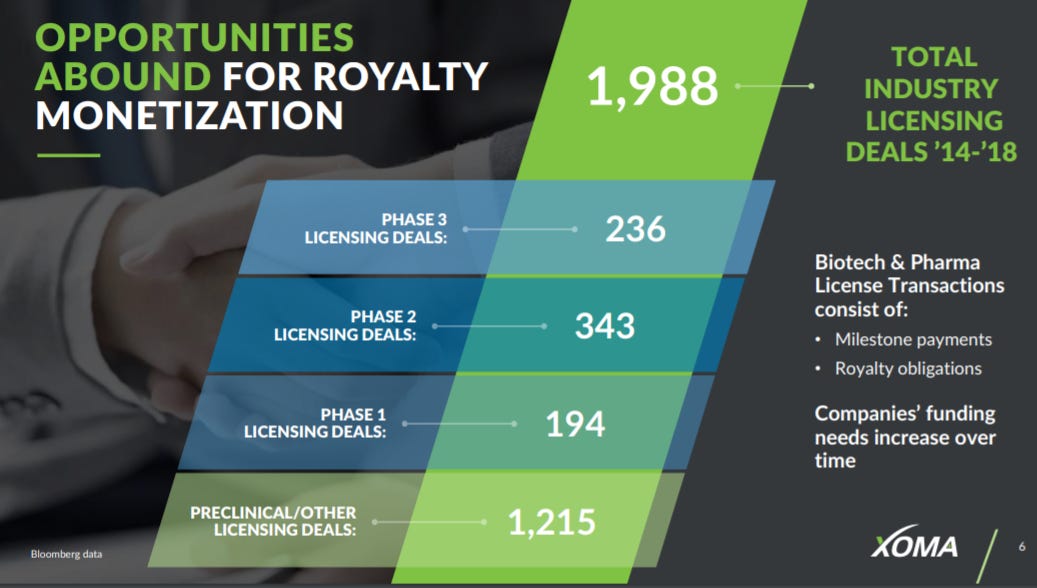

XOMA sizes the marketing opportunity for royalty aggregation: hundreds of deals to do per year.

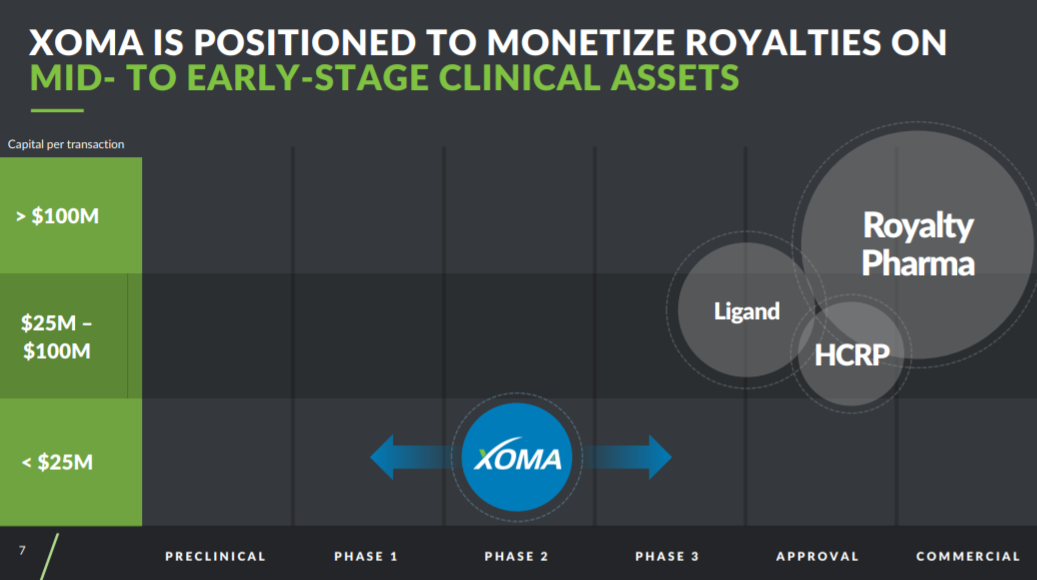

The next slide conveys XOMA’s market positioning as aggregating phase 1-3 clinical assets.

This positioning informs XOMA’s strategy to buy royalties on mid-stage clinical assets that may have more risk but can be purchases for smaller amounts of capital versus phase 3 and approved/commercial assets.

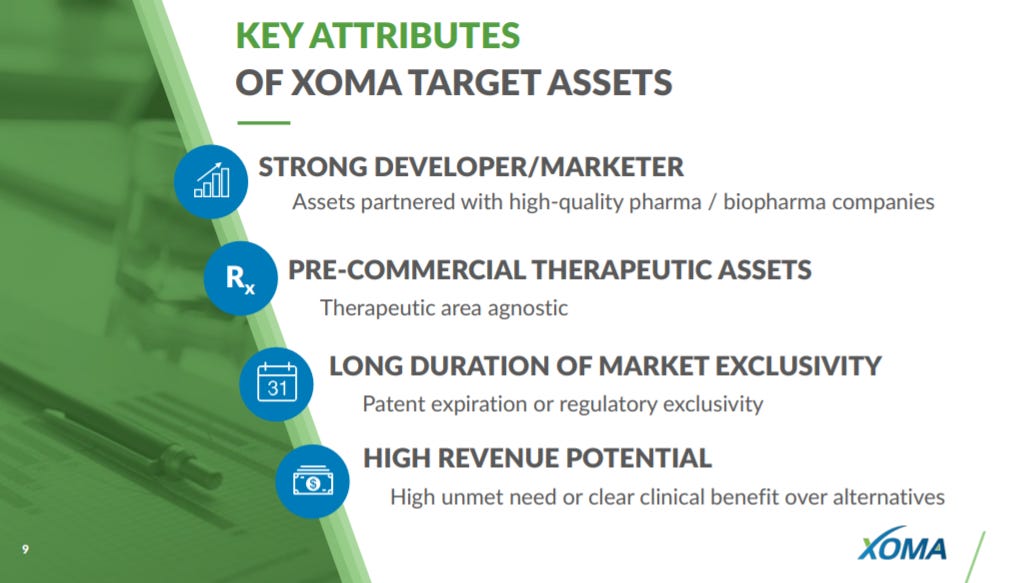

This slide gives an overview of the features for XOMA’s target assets: well capitalized biotech company developing the asset and blockbuster potential.

XOMA then gives a series of deal examples. The first one is their deal with Agenus for the company’s seven immuno-oncology assets it has partnered with Incyte and Merck on - https://www.prnewswire.com/news-releases/agenus-closes-15-million-partial-royalty-monetization-with-xoma-300716732.html XOMA paid $15M to Agenus to help the latter develop their own pipeline to gain access to up to $60M (for XOMA) in milestones and a royalty cut.

Another example is XOMA’s deal with Aronora for 5 hematology assets - https://www.globenewswire.com/news-release/2019/04/08/1798844/0/en/XOMA-Acquires-Royalty-Rights-to-Five-Hematology-Candidates.html

Another example is a deal with Palobiofarma for 6 assets around adenosine-receptor biology - https://www.globenewswire.com/news-release/2019/09/26/1921577/0/en/XOMA-Acquires-Royalty-Interest-Position-in-Six-Clinical-Stage-Assets.html

The last example of a XOMA deal with Chiesi Group for 4 assets for lysosomal storage disorders - https://www.globenewswire.com/news-release/2020/11/03/2119229/0/en/XOMA-Acquires-Royalty-Interest-in-Four-Lysosomal-Storage-Disorder-Enzymes-Being-Developed-Under-the-Chiesi-Group-Bioasis-Strategic-Alliance.html

XOMA ends the example slide series with a slide on how these deals fit their deal checklist.

The company goes into how to value XOMA’s portfolio of drug royalties - blockbuster potential combined with ~2% royalties = $100Ms in potential revenue to XOMA.

Then XOMA gives an overview of their portfolio: most are in phase 2 and are being developing by large drug development companies.

XOMA’s portfolio of drug royalties are pursuing a large set of diseases.

With XOMA making immuno-oncology their main focus.

XOMA then gives a quick snapshot of their portfolio with the partner, target, and royalty rates.

This slide goes into XOMA’s revenue potential. The company is essentially a bag of lottery tickets and if one hits, then the company will potentially generate $10Ms if not $100Ms in annual revenue.

XOMA’s strategy avoids their past strategy over the last ~4 decades: spend nothing on R&D and rely on unique financing structures to build a portfolio of promising clinical-stage medicines. XOMA could theoretically be completely virtual and maybe even automated in a capital-as-a-service format. If someone wants to build the software-first version of XOMA, please email me.

XOMA provides catalysts: payments from partners on legacy assets and building out the company’s portfolio of drug royalties.

XOMA’s penultimate slide repeats the last slide around catalysts and milestones.

The company ends with an argument for why XOMA is valuable: a large and diverse portfolio of drug royalties and low operational costs.

XOMA’s deck does a good job clearly conveying their business model of royalty aggregation and have made significant progress over the last 3 years since their pivot. As the company builds a larger portfolio of drug royalties and their balance sheet grows, XOMA’s cost of capital will go down driving scale and more cost efficiencies. There is an opportunity to aggregate royalties earlier and build a software-driven version of the business model

Follow up questions for the team:

What financing tools does XOMA use to raise capital in order to purchase drug royalties?

Can the royalties and payments due to XOMA from the company’s internal pipeline from its past biotechnology business be spun out into a separate entity (i.e. CVR)?

What is the status of XOMA’s antibody library? Who owns the rights? Can the antibodies be licensed out or used to build another company similar to Adimab or AbCellera?