Axial partners with great founders and inventors. We invest in early-stage life sciences companies such as Appia Bio, Seranova Bio, Delix Therapeutics, Simcha Therapeutics, among others often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you - email us at info@axialvc.com

Verastem Oncology was founded in 2010 to develop drugs against cancer stem cells. Verastem was formed about the work of 3 MIT scientists: Piyush Gupta (Whitehead Institute), Eric Lander (Broad Institute), and Robert Weinberg (Whitehead Institute):

The Epithelial-Mesenchymal Transition Generates Cells with Properties of Stem Cells - https://www.cell.com/fulltext/S0092-8674(08)00444-3

Identification of Selective Inhibitors of Cancer Stem Cells by High-Throughput Screening - https://www.cell.com/fulltext/S0092-8674(09)00781-8

The thesis at the time was that a small subset of cancer cells sustain a tumor and are the drivers for tumor recurrence and metastasis. As a result, Verastem initially worked to develop small molecules to inhibit signalling pathways thought to be essential for cancer stem cell survival and proliferation: FAK, PI3K/mTOR and Wnt. The cancer stem-cell hypothesis is still controversial within the oncology field, but this initial focus set up Verastem to raise the capital to eventually move toward KRAS mutant cancers.

The first slide of their latest corporate presentation lays out Verastem’s new business model - focus on KRAS (an important undruggable protein), early clinical data, and enough cash to last a few years.

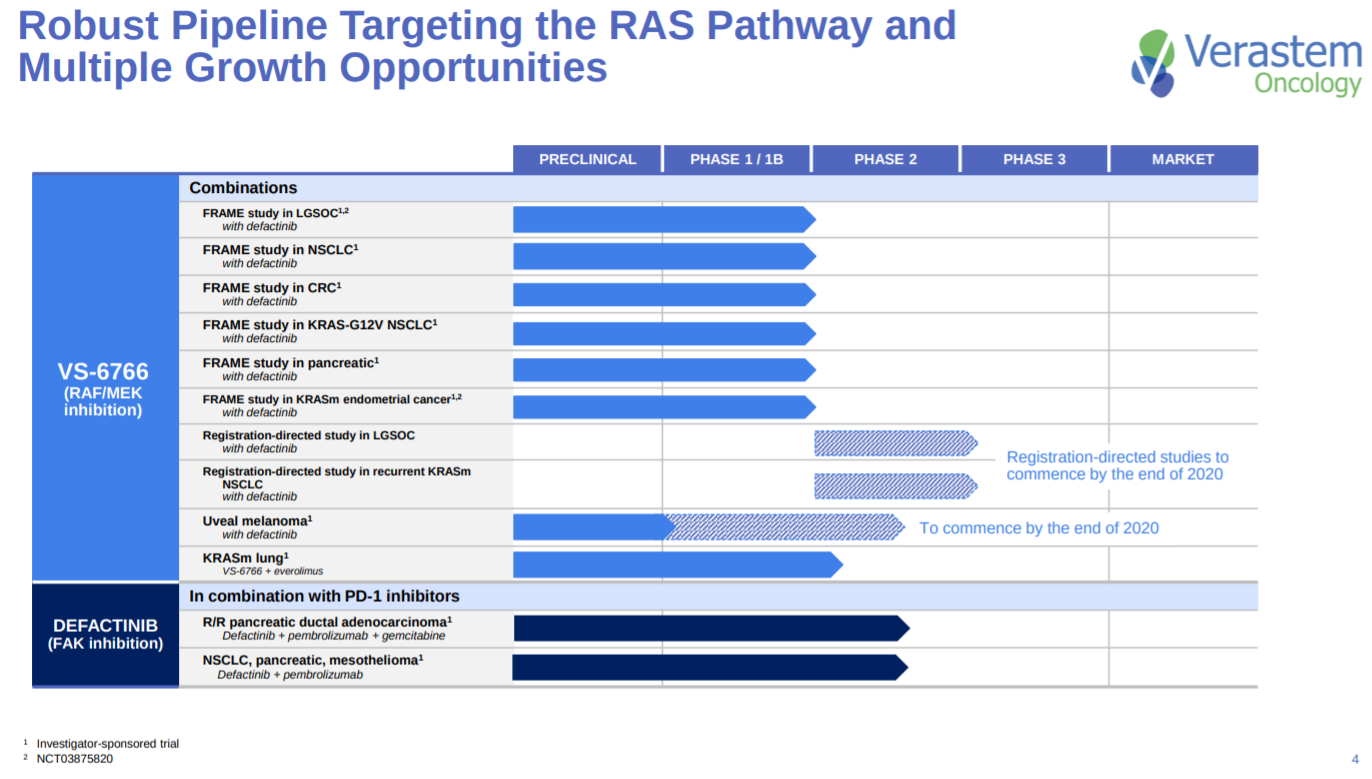

The next slide goes into their pipeline. One word: KRAS. VS-6766 is Verastem’s lead asset; the drug candidate is a dual RAF/MEK inhibitor that blocks both MEK kinase activity and the ability of RAF to phosphorylate MEK. The RAS/RAF/MEK/ERK pathway is activated in many cancers and is important and leads to gain-of-function mutations in the KRAS, NRAS or BRAF genes. They still have their FAK inhibitors from their past focus in cancer stem cells.

Verastem is pursuing a combination strategy of their FAK inhibitor, defactinib, with VS-6766 in gynecological cancers. FAK (focal adhesion kinase) is a non-receptor tyrosine kinase that mediates signaling downstream of integrins and growth factor receptors, and regulates cell survival, proliferation, migration, invasion, and adhesion. FAK is overexpressed in many tumor types particularly in cancers that have high invasive and metastatic capability.

They then give an overview of LGSOC - a rare ovarian cancer subtype that affects younger women.

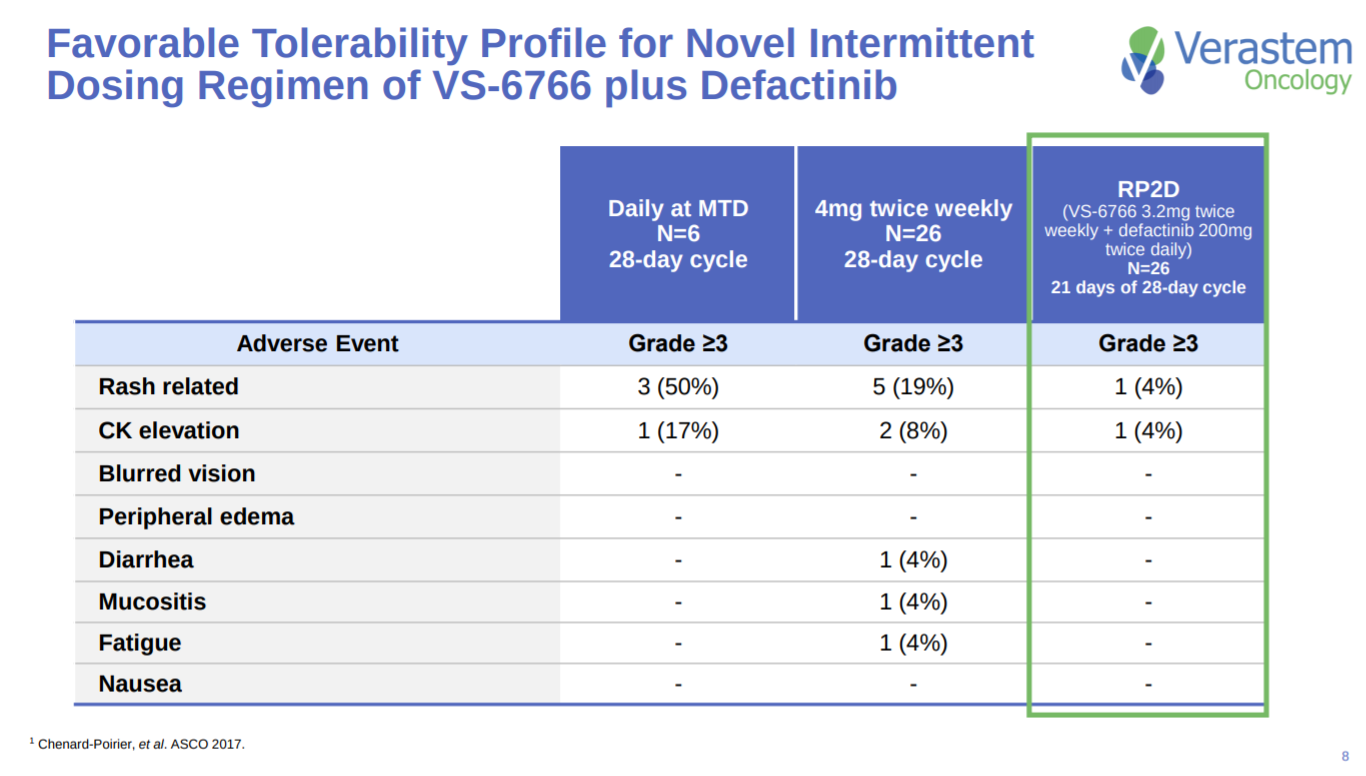

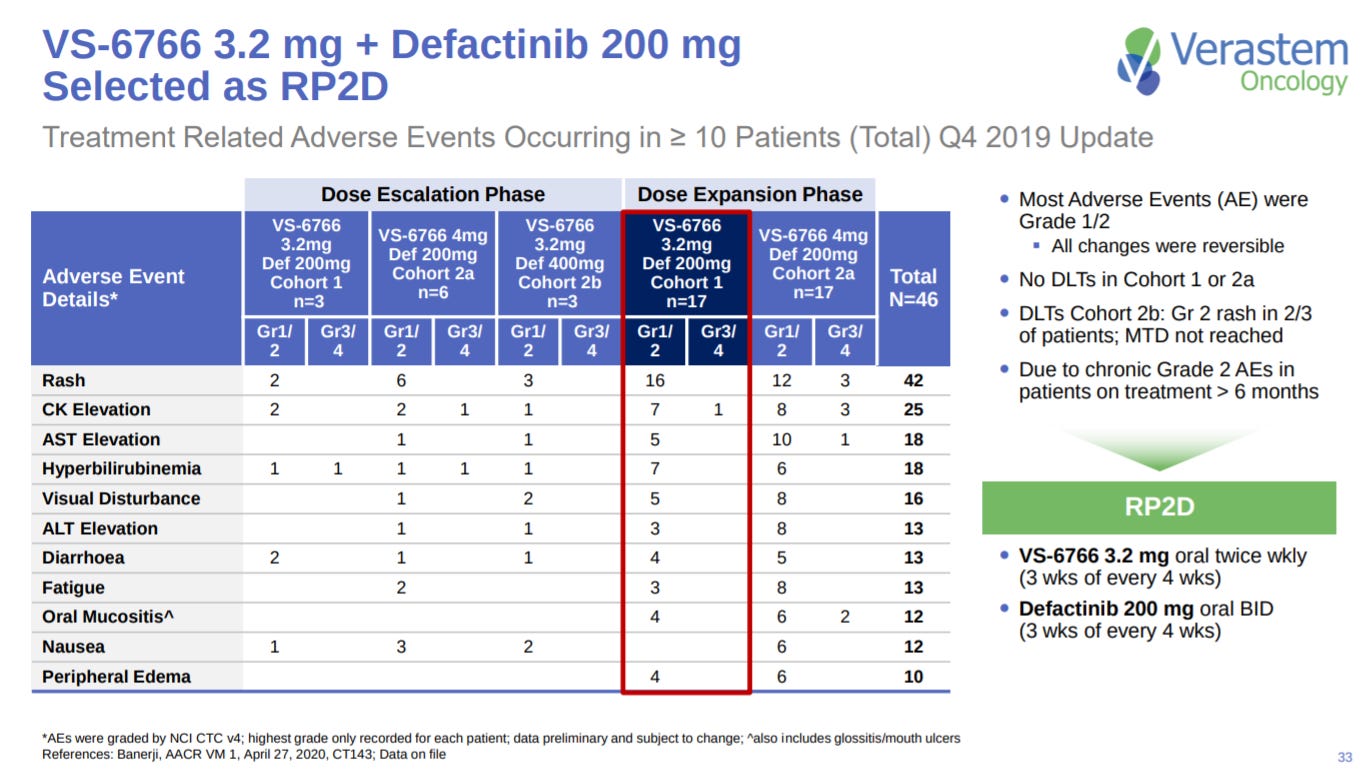

After laying out their pipeline and lead indication, Verastem shows safety data for the combination of VS-6766 and defactinib.

Early efficacy in LGSOC shows promise with an ORR above 50% for patients with a KRAS mutation.

The ORR is still maintained at dose levels they intend to use for the phase 2 trial.

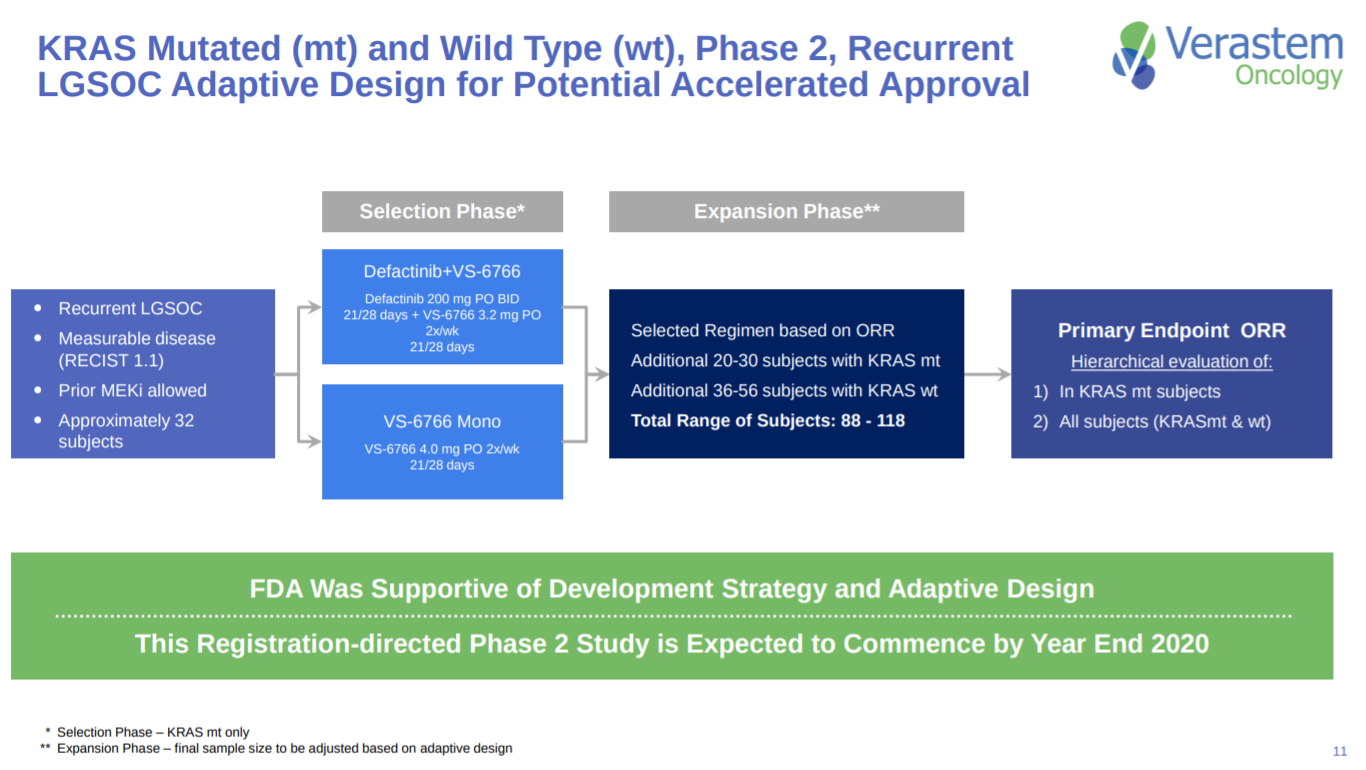

With this data, Verastem shows the design of the phase 2 trial for the combination therapy in LGSOC. The focus is on responses in patients with KRAS mutations.

After showing their data in low-grade serous ovarian cancer, Verastem goes into the market opportunity.

Around a third of LGSOC patients have a KRAS mutation. With the disease being a rare cancer.

With LGSOC patients having some unmet need - better medicines are needed especially since the disease onset takes years.

This slide wraps up the advantages for Verastem’s lead asset and their next steps to move into a phase 2 trial.

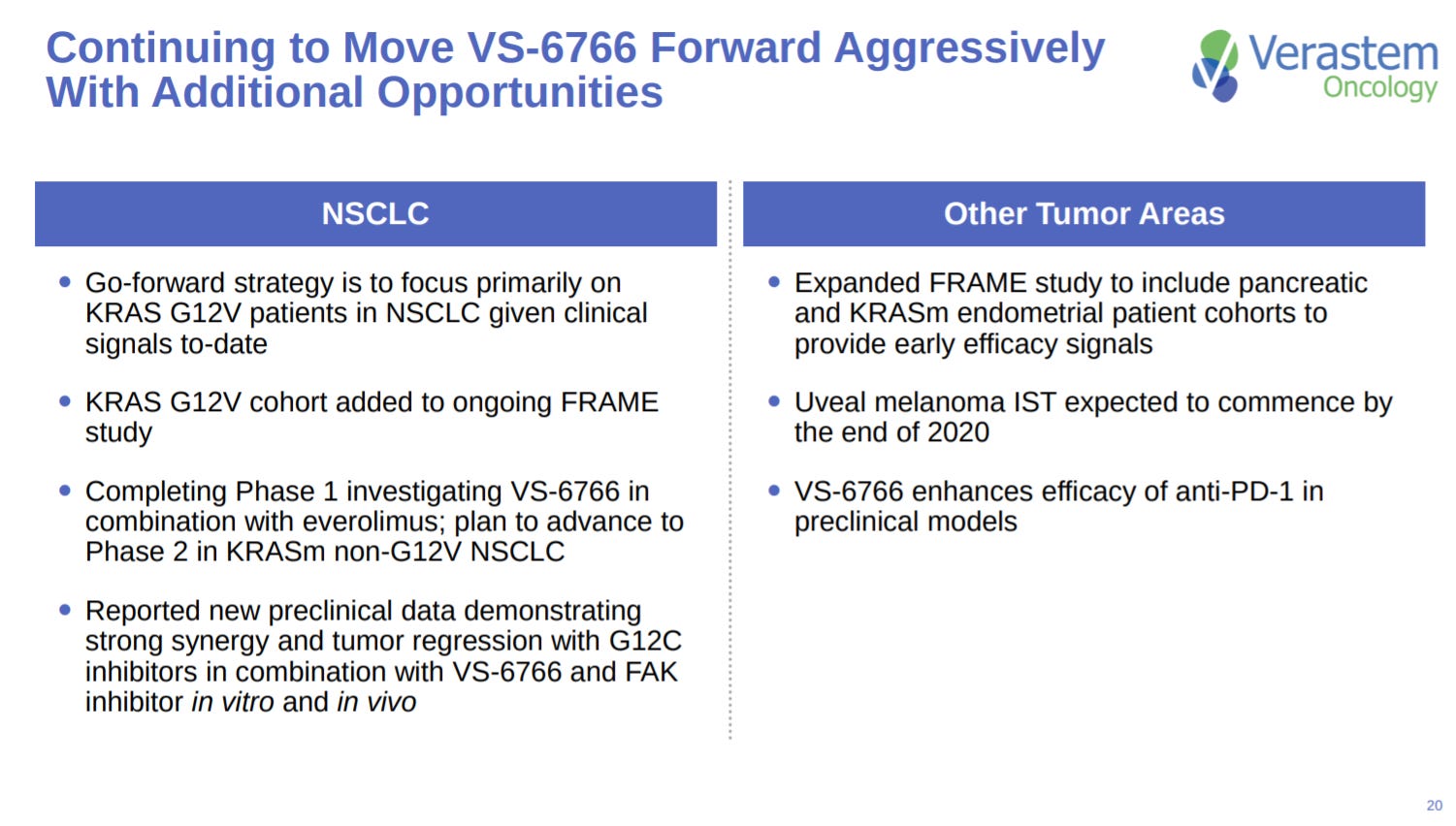

The company also gives updates on their other programs. There is a large opportunity to treat KRAS mutant NSCLC.

For KRAS-driven NSCLC, Verastem shows data on ORRs and treatment times for certain KRAS subtypes.

The next slide describes the design of phase 2 trial in NSCLC.

This slide synthesizes the last two slides. Maybe Verastem should just focus on LGSOC solely and partner off other assets down the line.

The pipeline slide again?

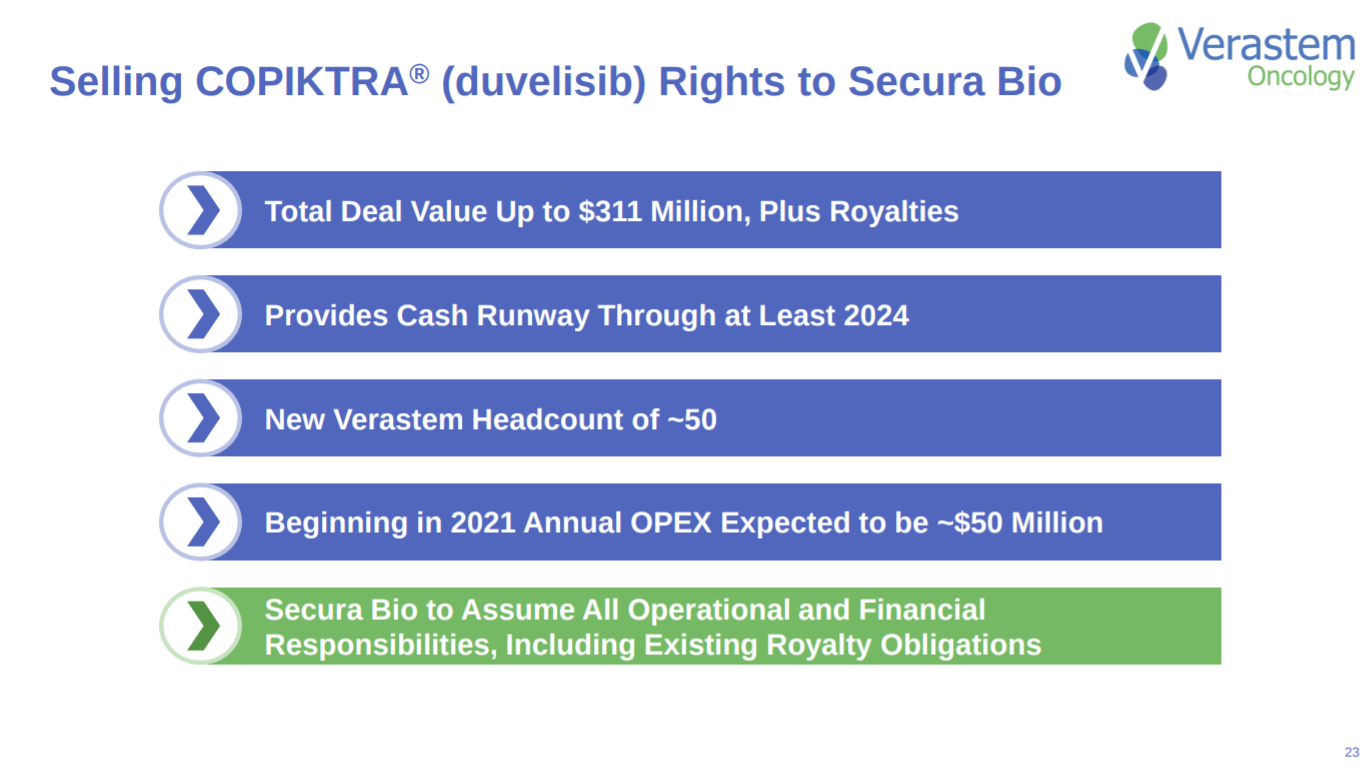

Near the end of the presentation, the company describes their recent sale of Copiktra to Secura Bio. Verastem sold the rights of their approved oral inhibitor of phosphoinositide 3-kinase (PI3K) in CLL and SLL to Secura Bio. Verastem received $70M along with milestone payments and low double-digit royalties on net sales over $100M in the US and Europe. Verastem had to execute the deal to raise more cash after their recent lung cancer data showed poor efficacy.

The penultimate slide gives an overview on Verastem’s financials. Enough cash to move their lead program into phase 2 trials.

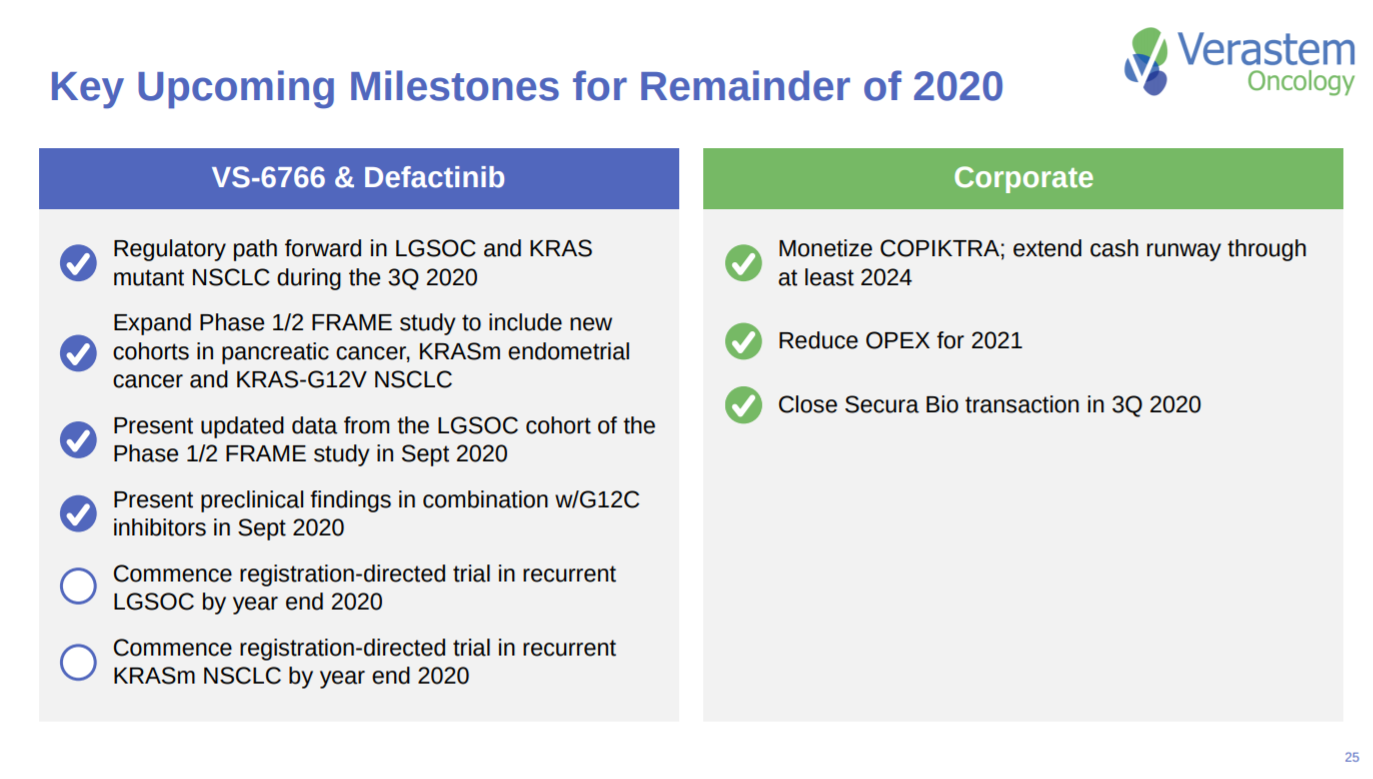

The last slide goes into the company’s milestone they have achieved.

The next series of slides are part of the appendix.

Cancers driven by the RAS/RAF/MEK/ERK pathway have a lot of unmet need. A massive opportunity for any cancer company in general to make an impact on patient lives.

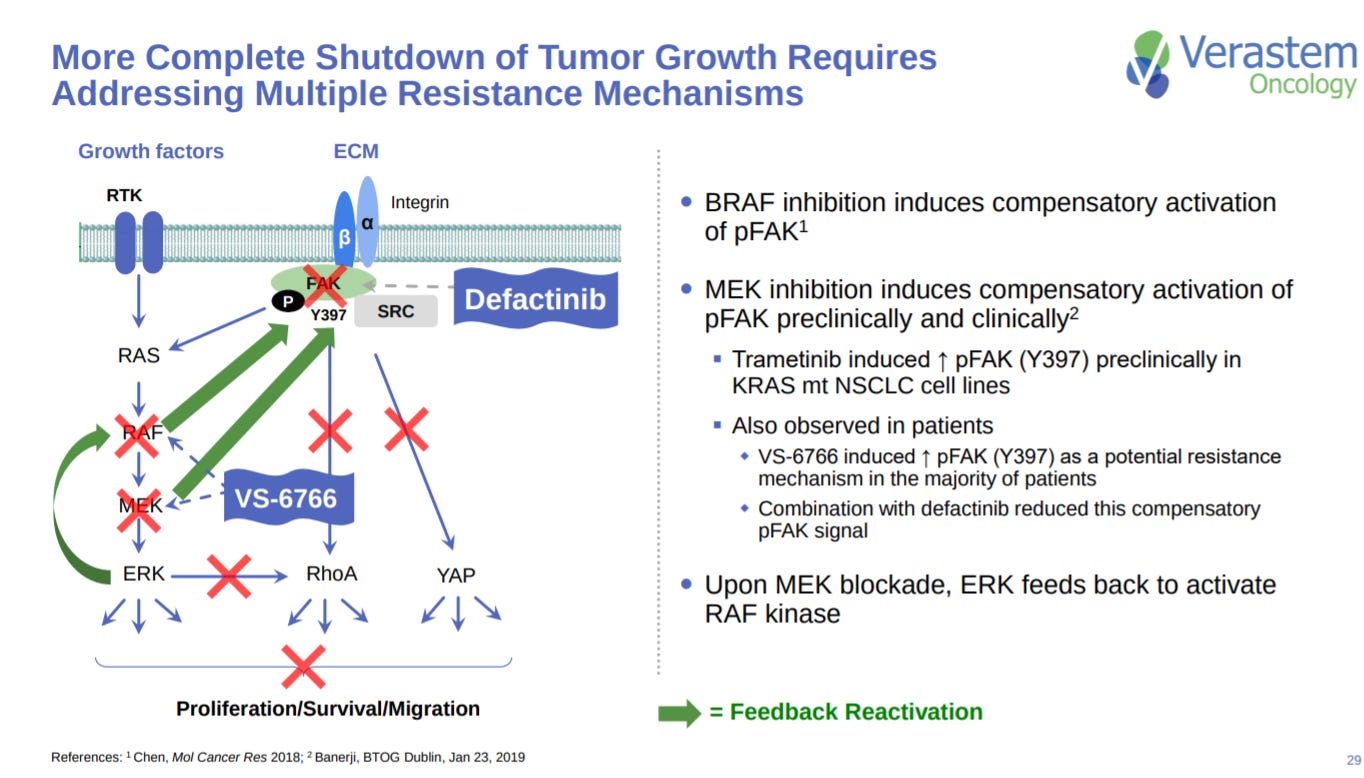

This slide gives an overview on VS-6766 mechanism: dual inhibition of RAF and MEK.

Building on the last slide, the MoA focused on inhibiting RAF and MEK to prevent FAK activation.

VS-6766 is also a CRAF inhibitor, an important oncogene of RAF.

Verastem shows early data on the potential synergies to combine VS-6766 and KRAS (G12C) inhibitors. This data is really early, but could enable a lot more business model flexibility (i.e. partner with Amgen on their KRAS program).

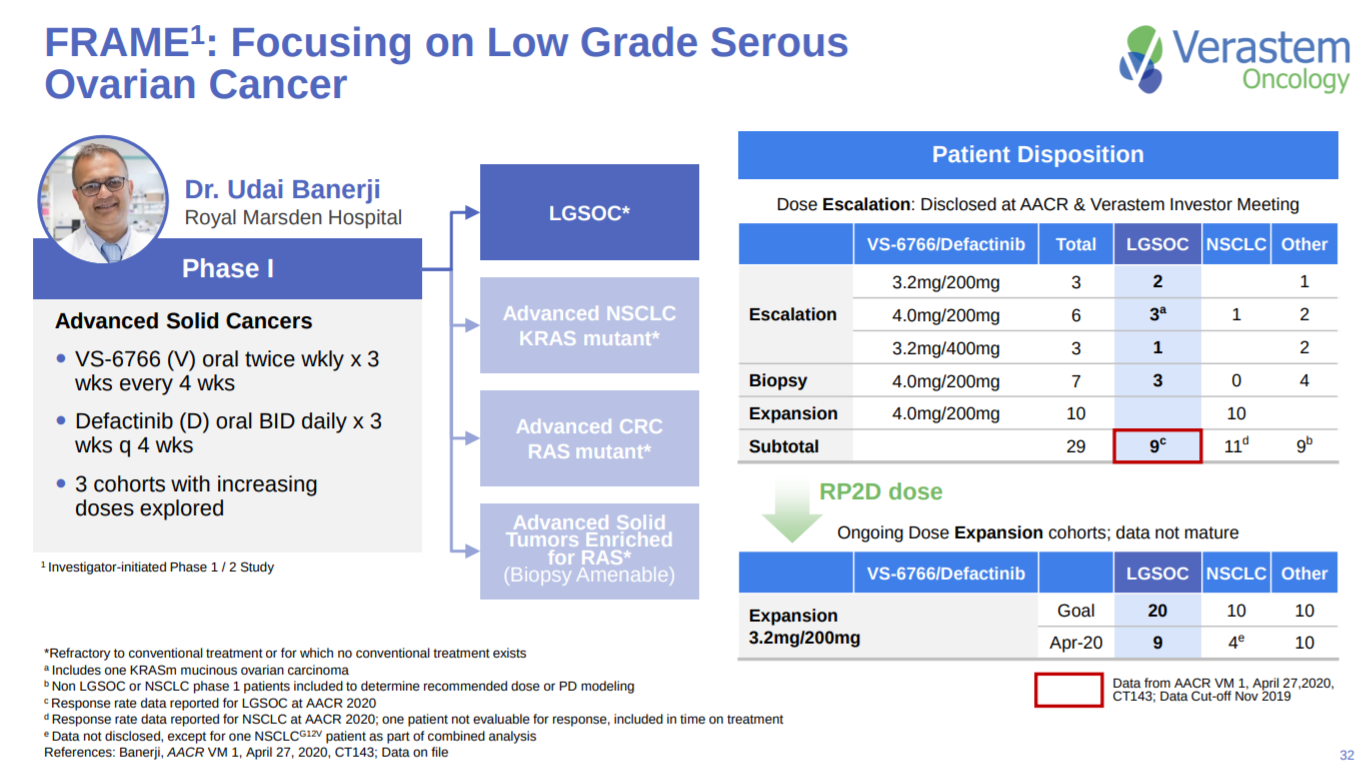

In LGSOC, the company lays out their patient recruitment strategy

With a dose expansion to determine a safe dose for their phase 2 trial.

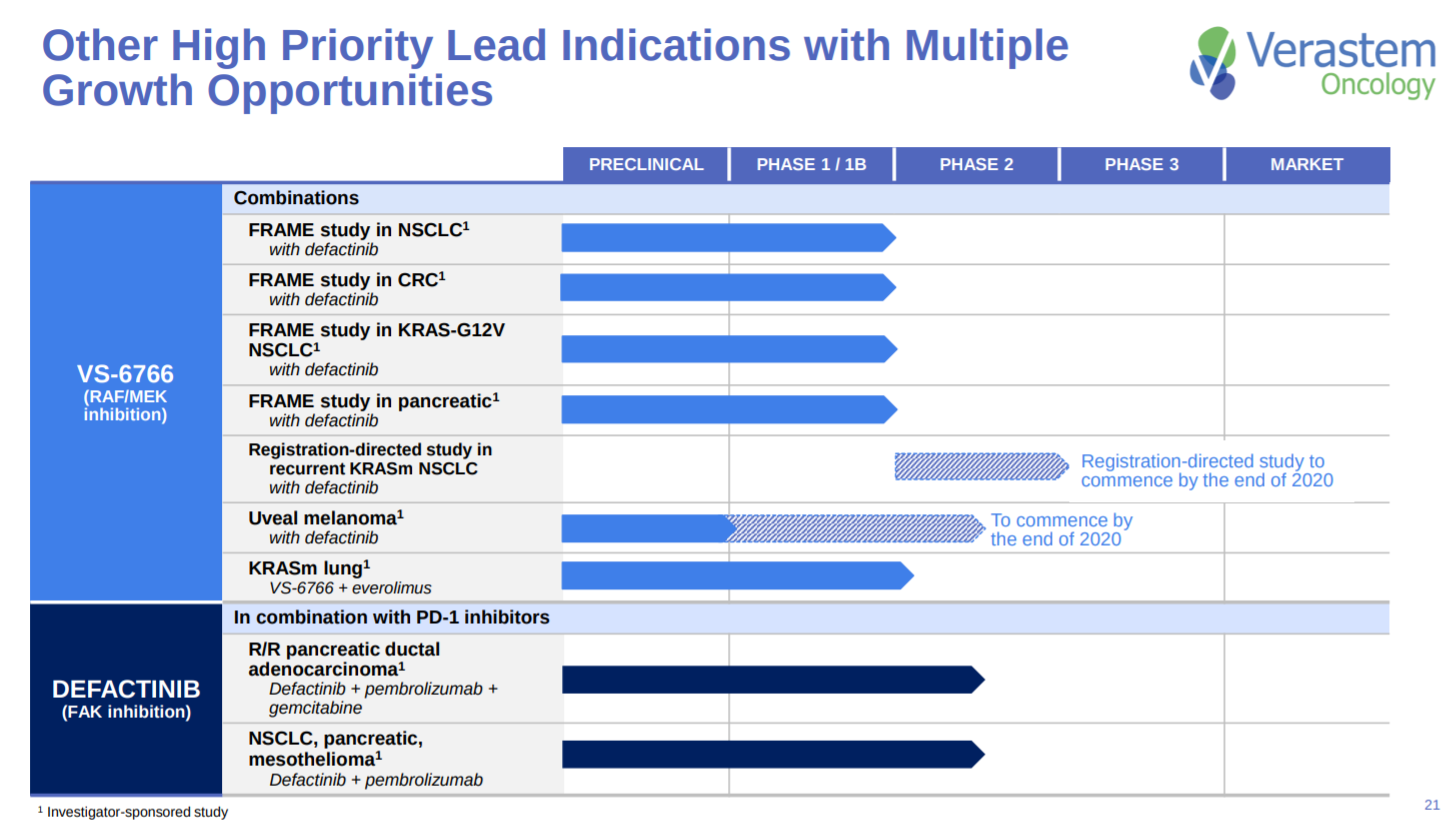

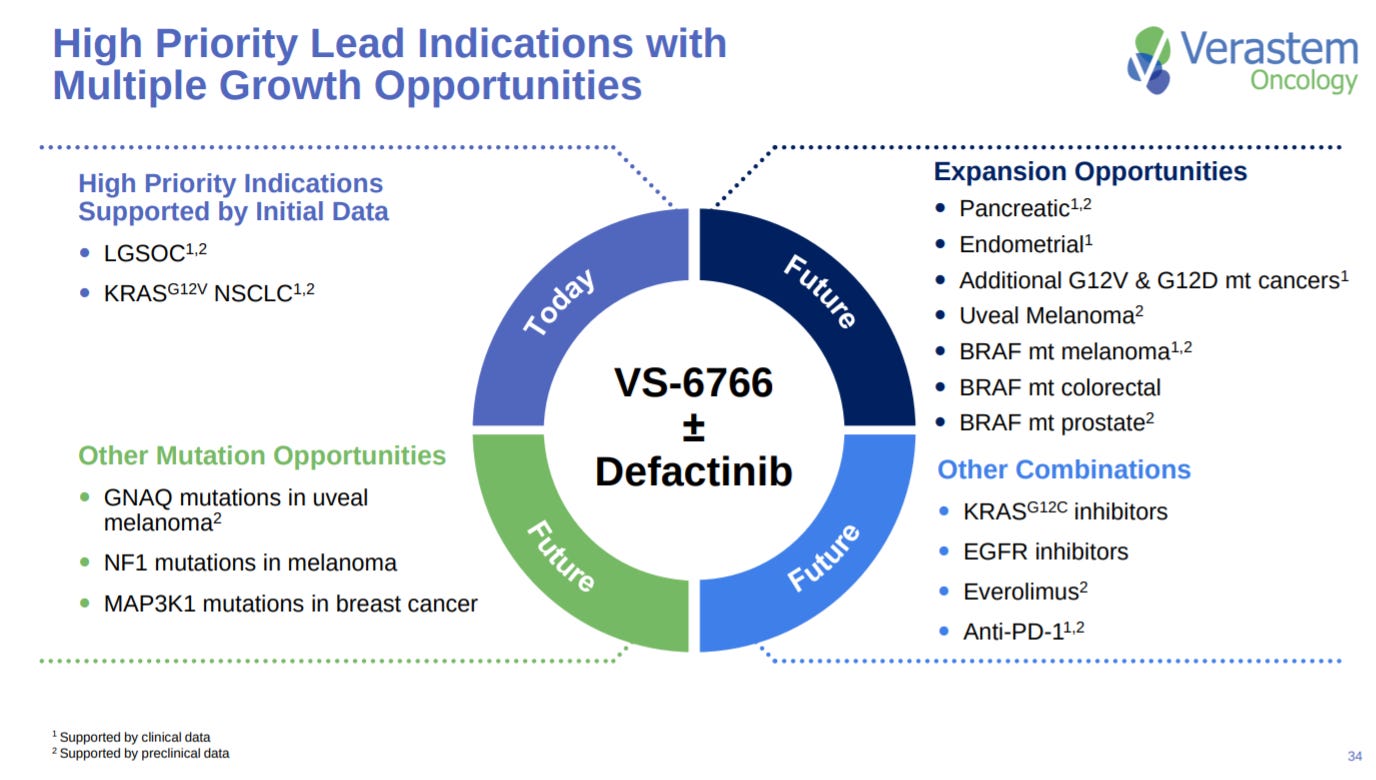

This is an important slide on the next indications VS-6766 with defactinib can address.

The last slide goes into Verastem’s executive team. Pretty standard.

Verastem’s presentation shows the opportunity to develop new medicines for the RAS/RAF/MEK/ERK pathway and describes their lead programs in LGSOC. However, they need to do a better job differentiating their work as well as putting their data in context with previous failures.

Follow up questions for the team:

Will Verastem receive an exemption from the FDA in LGSOC since the patient population is relatively small?

Why is the company still pursuing the NSCLC program?

What business development opportunities exist? Any exploration around combining VS-6766 with KRAS inhibitors? SHP-2?