Deck Review with BridgeBio

Surveying great inventors and businesses

Axial partners with great founders and inventors. We invest in early-stage life sciences companies such as Appia Bio, Seranova Bio, Delix Therapeutics, Simcha Therapeutics, among others often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you - email us at info@axialvc.com

BridgeBio is a superforecaster in medicine. With a growing outsider moat in drug development, the company has the potential to become a Danaher or Constellation type of business model. With this framing, BridgeBio not only has the potential to bring transformative medicines to patients but to raise the bar for efficiency in the industry. Some key themes for BridgeBio are:

Focusing on specific fields or classes of medicine that have had high amounts of research financed by other people and a rich history, and use this record to become a superforecaster (i.e. curation and management) in the clinic

Relying on 3 key parts: financing (i.e. from unique sources), portfolio (i.e. multiple shots on goal), and curation (i.e. discipline).

The BridgeBio model is reliant on a small internal team and distributed development need a strong system and playbook to share across their network to maintain quality and discipline

The first slide of their latest corporate presentation clearly states BridgeBio’s mission to bring new medicines to patients genetically-driven diseases focusing on rare diseases and cancer.

The next slide is very powerful. Using the Day 1 phrase Jeff Bezos uses for Amazon, the company shows the increasing power of sequencing has driven growth of not only genetic variants driving monogenic diseases but common diseases like diabetes and cardiovascular too. This slide suggests the BridgeBio’s vision is to pursue much larger indications in the future.

This slide then sizes up the opportunity for treating genetic diseases relatively to other indications. A caveat here is unmet need.

After laying out the opportunity BridgeBio is pursuing, the company explains it’s strategy to focus on diseases with genetic drivers. I am a big fan of the strategy book, but it might be better to show some data showing improved odds of clinical success for genetically-defined indications.

Sticking on the theme of referencing a book, the company completes its vision by saying that scale will come from a decentralized model similar to Danaher.

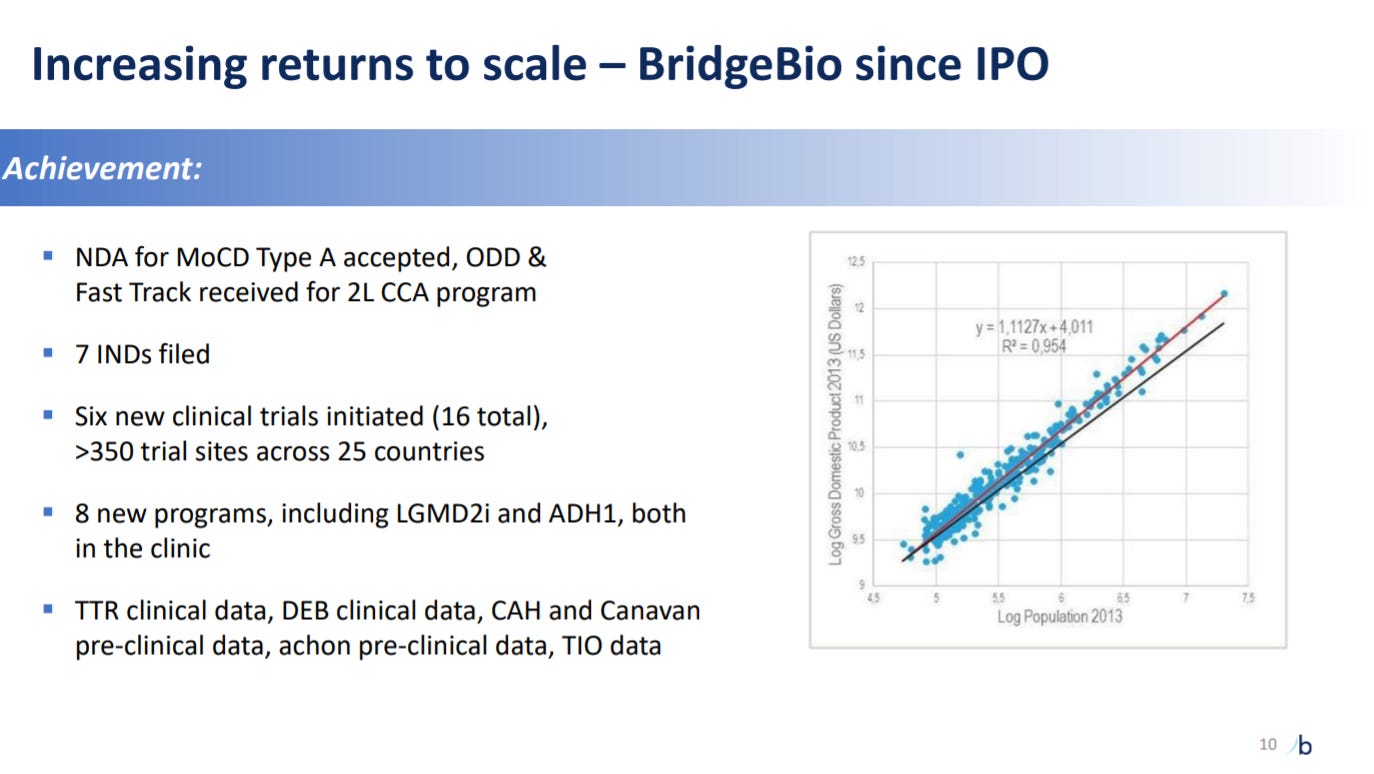

The company starts going into its progress. The last five years has been truly amazing for BridgeBio.

The next slide is a little confusing but BridgeBio is using GDP/Population plots to prove that scale for the company will bring more products and growth.

Then then go into their platform: (1) Discover the genetic driver for a given disease (2) Pick a modality for the target (3) Bring the drug candidate through the clinic and finance this work appropriately (4) Commercialize their own product. The fully-integrated model.

For the first step of the platform, the company relies on research partners and genomics to discovery and validate targets.

On top of that, they have a pretty awesome bench of scientific advisors to help with target selection.

Once a target is figured out for a disease, Bridge Bio is modality agnostic. This means to have to ingest a lot of IP for this like ASOs and AAV gene therapies once they need them.

They have another bench of advisors with expertise in drug development to help with the modality choosing process.

For the clinical stage, this slide is very important because it suggests that BridgeBio will benefit from economies of scale in terms of clinical operations with more trials initiated.

The last slide on their platform is around commercialization, which I assume they are still laying out their plans for. But BridgeBio is relying on external partners to commercialize drugs in certain countries and patient advocacy groups to make sure their medicines get to the right people.

The first 3 parts of their platform have grown significantly over the last 5 years with the commercialization part coming up over the next 1-2 years.

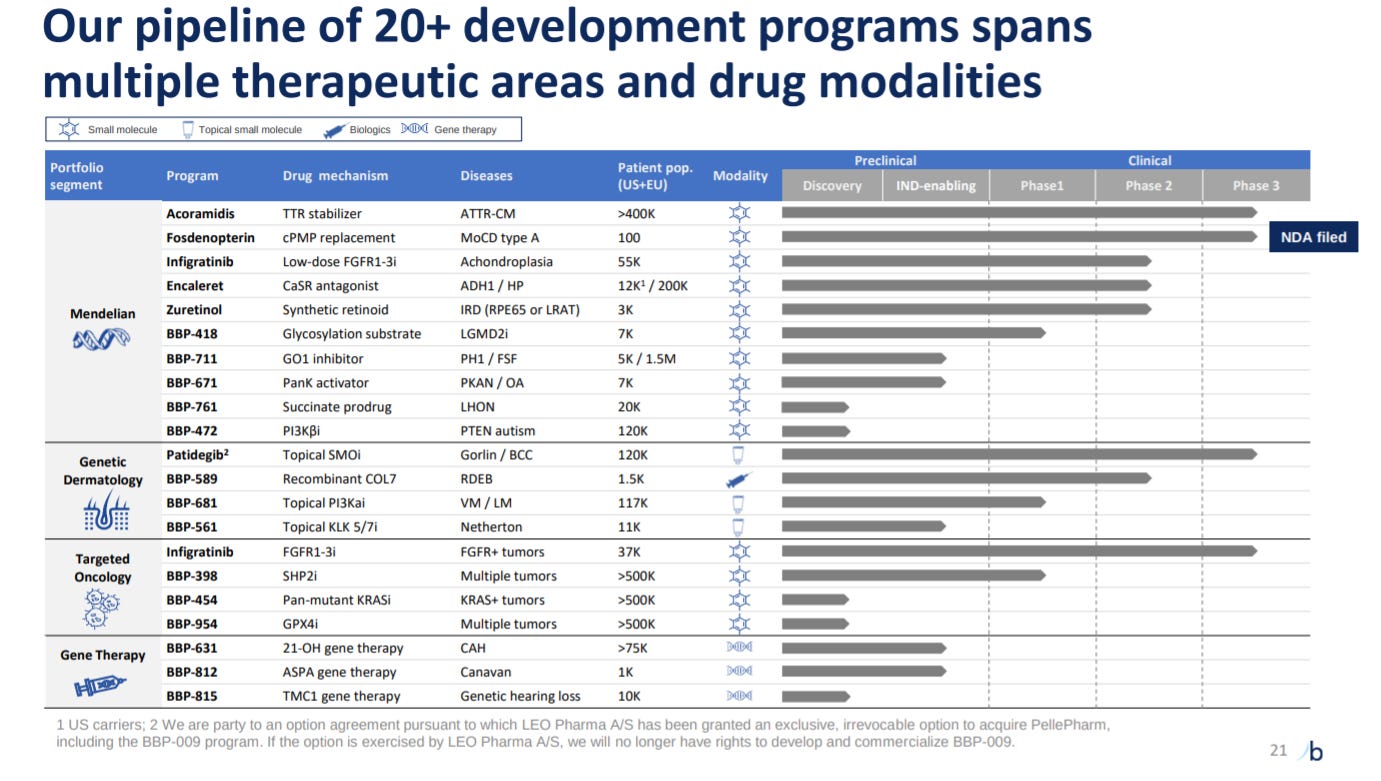

This slide goes over their pipeline. For BridgeBio, overlaying their pipeline slide with capital structures for each asset would be very useful.

Before going into their pipeline, BridgeBio explains their milestones. They also lay out their milestones at the end of the presentation.

BridgeBio once again reiterates how valuable their current pipeline is.

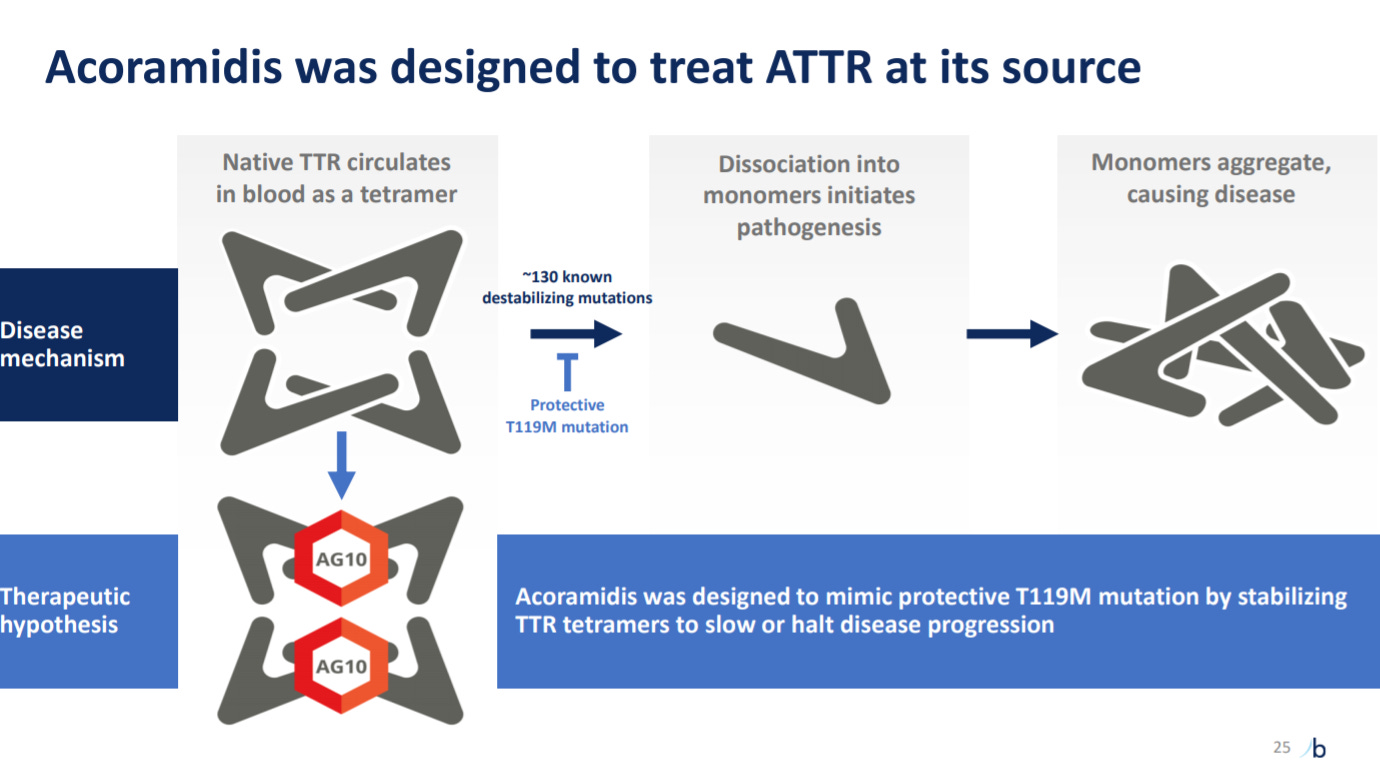

One of BridgeBio’s most well-developed drug candidates is for ATTR, an inherited disease where a mutant-form of transthyretin misfolds and forms fibrils aggregating in various organs and nerves.

BridgeBo’s AG10 drug candidate for ATTR is focused on mimicking a protection mutation to lock TTR in a tetramer and prevent fibrils from forming.

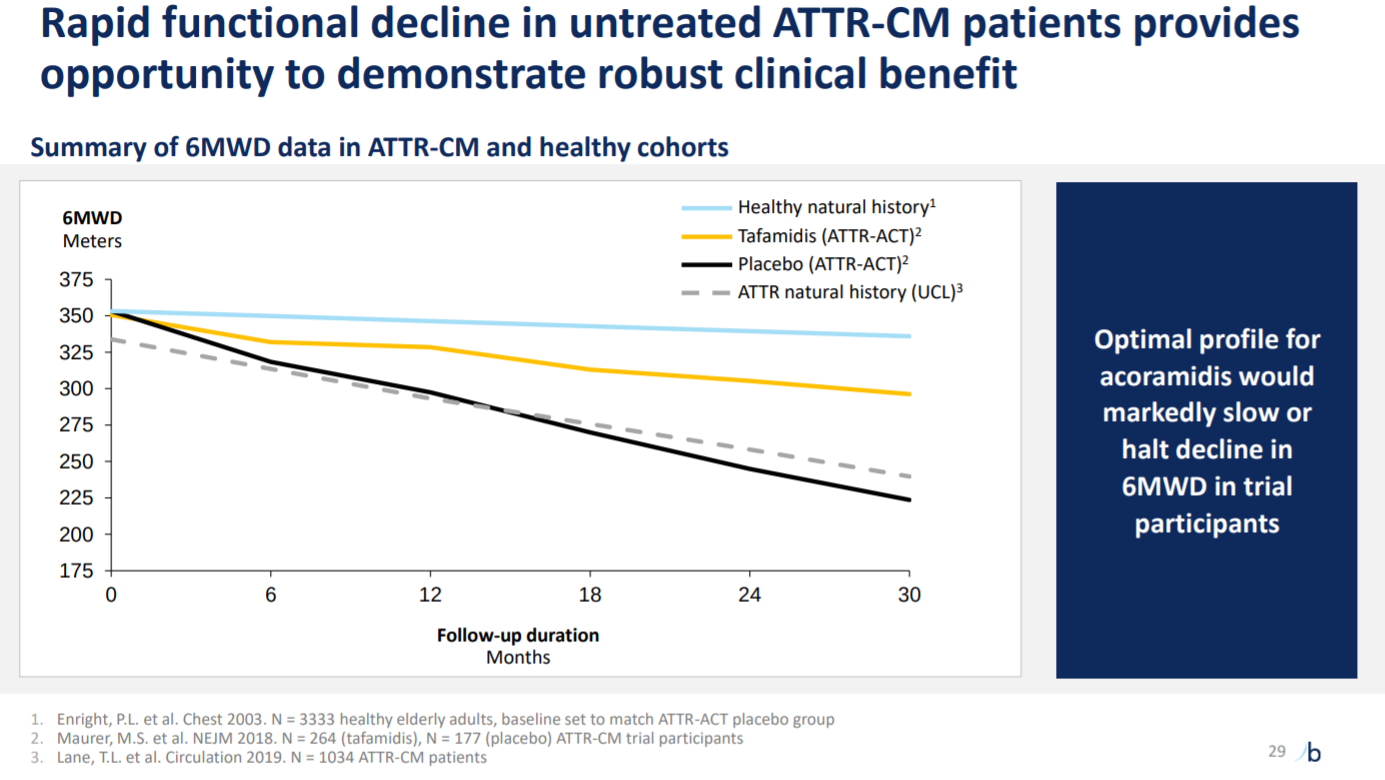

After explaining their logic for treating ATTR, the company shows pretty strong safety data in their phase 2 trial.

Then BridgeBio maps out their phase 3 trial design for AG10 with inclusion/exclusion criteria and two primary endpoints: 12 months for 6 month walking distance and 30 months for mortality.

This is a another slide to explain the trial’s endpoints.

For the 6 month primary endpoint, AG10 ideally shows non-inferiority to another approved medicine for ATTR-CM: Tafamidis.

For the 30 month primary endpoint, BridgeBio will compare the treatment and placebo arms in a pairwise method with mortality ties broken by cardiovascular hospitalization rates.

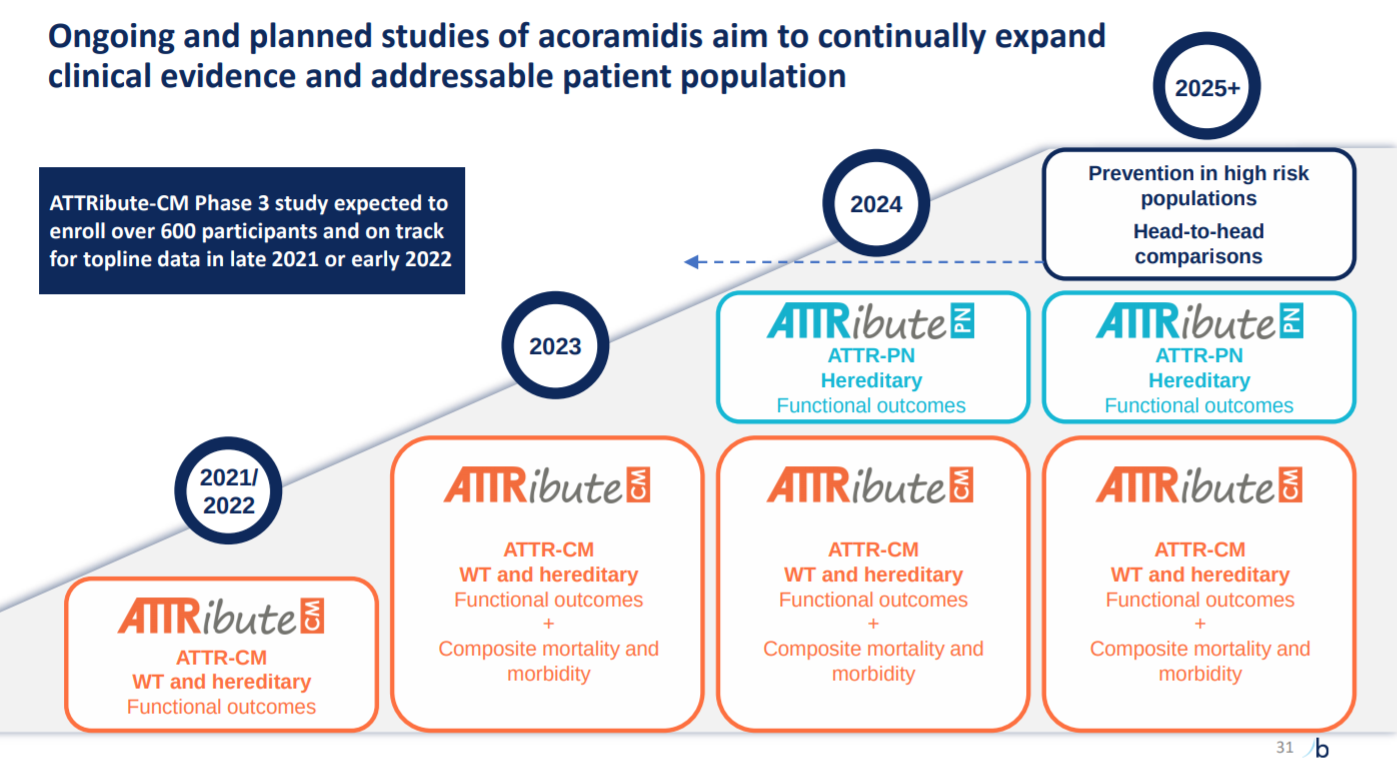

With this clinical plan for phase 3 in ATTR-CM, the company will generate pivotal data in ~3 years and expand to ATTR-PN.

The presentation has slides on a few other programs and ends with various milestones/catalysts for the company over the next 1.5 years.

The deck does a great job at presenting the opportunity to treat genetic diseases but could do better at highlighting some of BridgeBio’s advantages. The topline data for the AG10 program in 2021/2022 is exciting along with their expansive pipeline.

Follow up questions for the team:

What logic does BridgeBio use to figure out whether to acquire a spinout or keep it independent? Eidos Therapeutics in ATTR is the latest example for the company.

Will the business pursue or sponsor large-scale sequencing efforts for complex diseases? How will academic collaborations be scaled up?

In combination with 2, what indications are on BridgeBio’s roadmap? How is sufficiency determined that a disease is understood well enough genetically for BridgeBio to pursue?