Deck Review with Aravive

Surveying great inventors and businesses

Axial partners with great founders and inventors. We invest in early-stage life sciences companies such as Appia Bio, Seranova Bio, Delix Therapeutics, Simcha Therapeutics, among others often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you - email us at info@axialvc.com

Aravive was founded in 2007 to develop new medicines in oncology and now has a pipeline targeting the GAS6-AXL signalling pathway, which is important for tumor growth and migration. AXL is a receptor tyrosine kinase while GAS6 is its ligand. AXL’s link to cancer was discovered in 1988, and since 2018, several new studies have suggested the potential for drugging the pathway in combination with other medicines.

However, the mechanism of AXL overexpression in cancer cells is still not fully understood, but the pathway is thought to reduce immunosurveillance and allow for cancer resistance. In addition to Aravive, companies like Mirati Therapeutics, Astellas, Exelixis, Eli Lilly, Genmab, Incyte among others have new drug development programs targeting GAS6-AXL signalling in cancer as combination therapies.

Aravive’s lead asset is AVB-500, a soluble Fc-fusion decoy receptor for GAS6. The strategy is to deplete AXL of its ligand and block activation of the pathway. The company’s strategy is to combine the drug candidate with other cancer drugs based on the data that has been coming out since 2018. With some early success, the company has the potential to execute a pipeline-in-a-pill strategy centered around GAS6-AXL signalling.

The first slide of their latest corporate presentation uses a clever figure to orient Aravive around halting tumor growth.

The next slide goes into the company’s team and board. Raymond Tabibiazar founded Aravive, which was originally named Ruga and was in stealth mode for a pretty long time until 2016.

The company adds a slide on their cap table to probably show that Invus is a significant investor. Moreover, Raymond still owns a little over 6% of the company.

This slide conveys Aravive’s focus - cancers driven by GAS6-AXL.

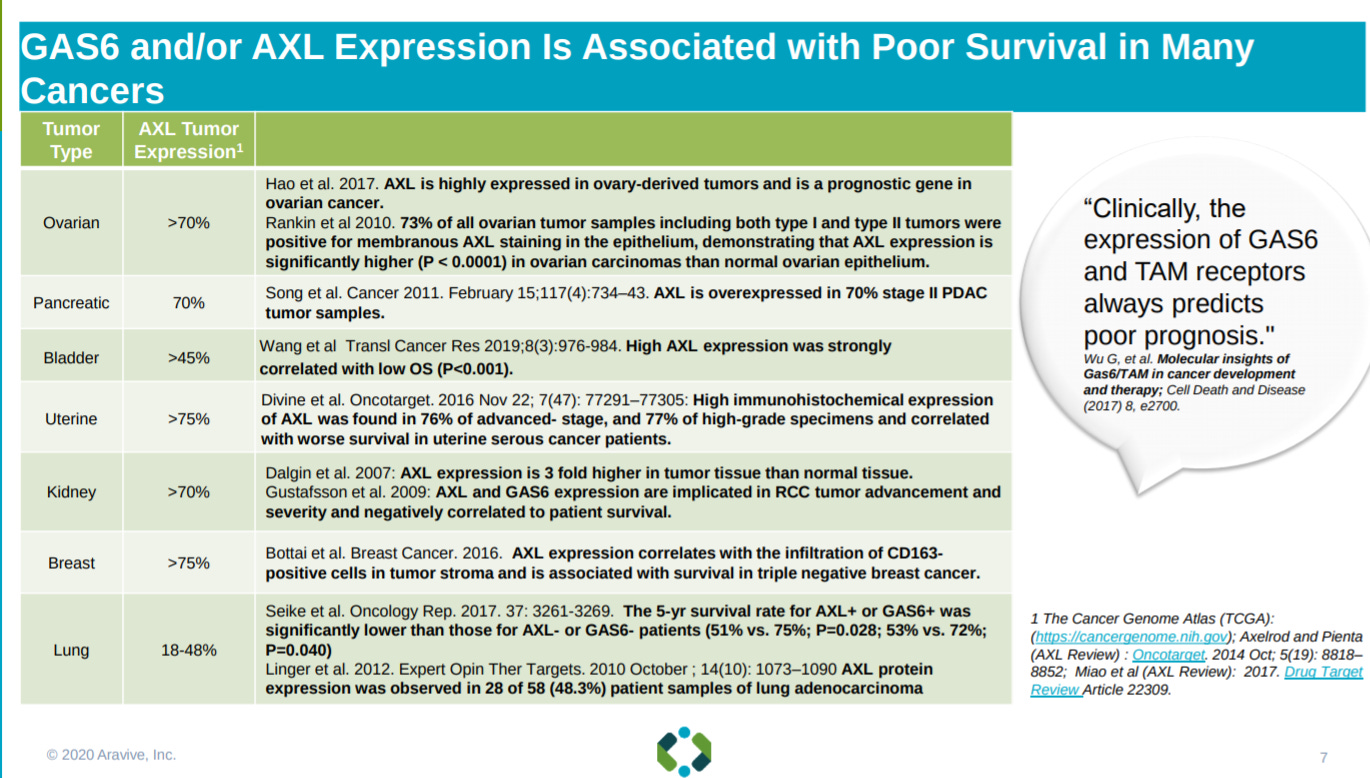

The next slide goes into the GAS6/AXL MoA - the genes are overexpressed in many cancers driving growth and resistance. GAS6 is the activating ligand for AXL.

This MoA is associated with a wide-range of solid tumors.

Aravive’s strategy is to use a biologic that acts as a decoy receptor to suck down GAS6 so it cannot activate AXL. What makes Aravive’s lead program, AVB-500, unique is its selectively to target only AXL signalling and avoid other receptor tyrosine kinases.

This slide gives an overview of Aravive’s lead asset with the focus on combining it with other medicines.

The first indication for AVB-500 is platinum resistant ovarian cancer.

Data from the phase 1 trial of AVB-500 in PROC showing tolerability in patients.

The next slide explains the design of the phase 1 trial.

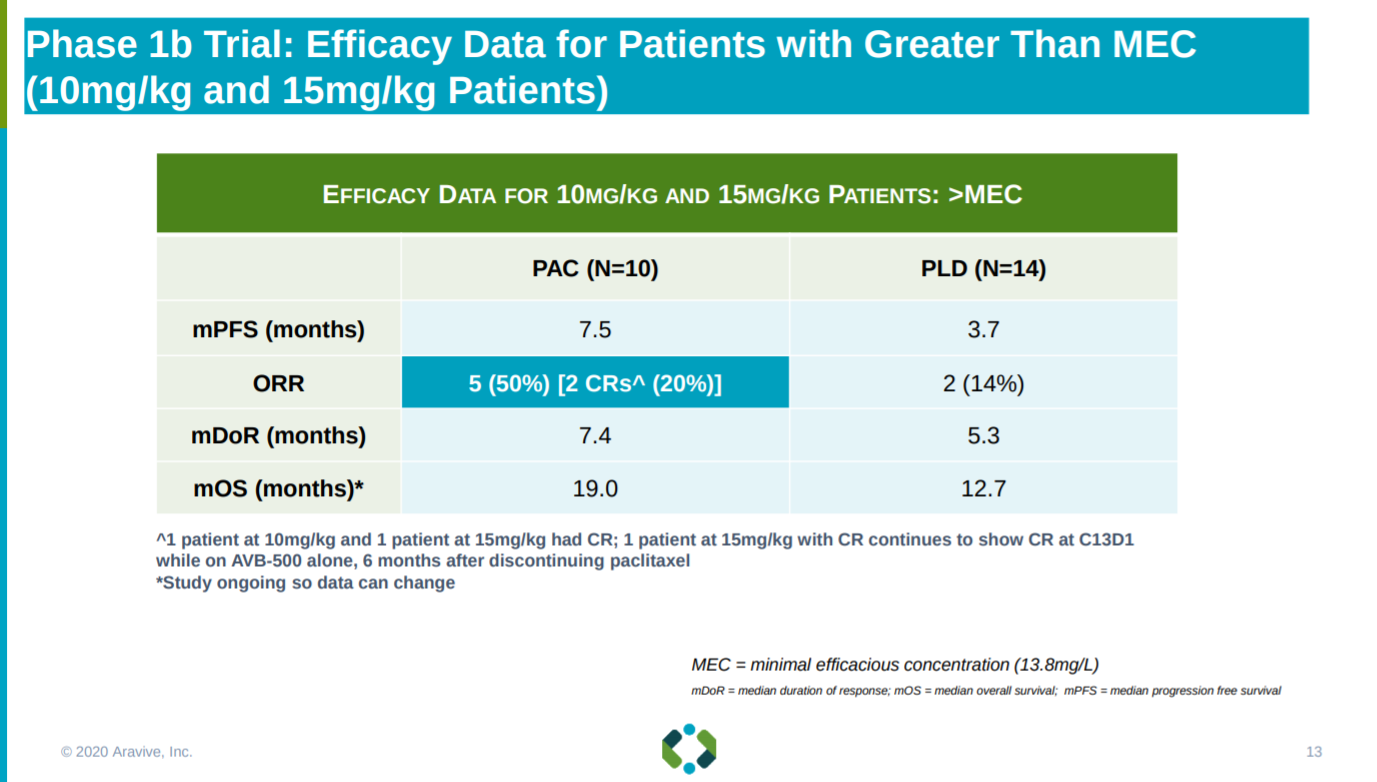

With early efficacy signals of AVB-500’s combination with paclitaxel (PAC) but not pegylated liposomal doxorubicin (PLD) in terms of overall response rate (ORR) and median progression-free survival between than the standard-of-care, Mitoxantrone, Etoposide, and Cytarabine (MEC), in PROC.

With similar efficacy signals for AVB-500 and PAC for patients that have not taken Bevacizumab (Avastin; antibody targeting VEGF-A) before.

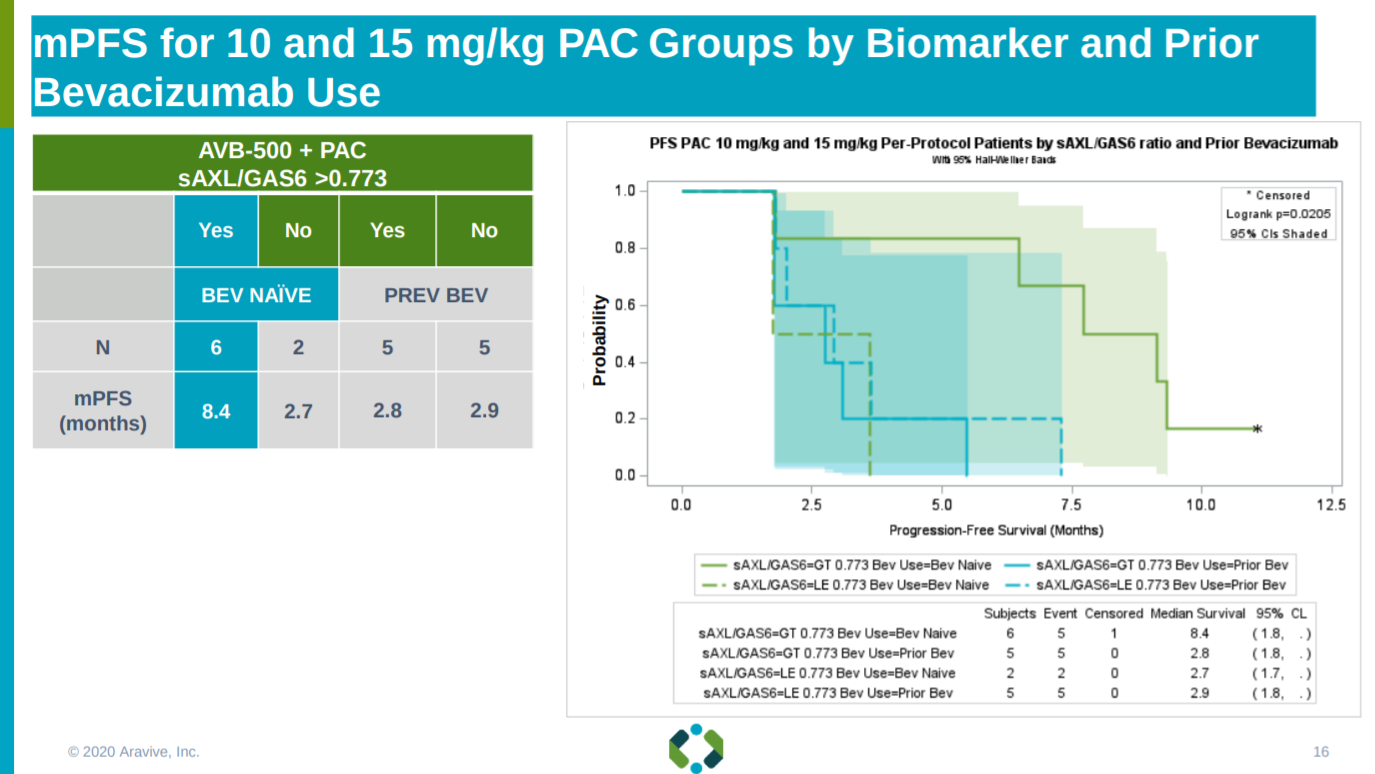

From the phase 1 work, Aravive found a potential biomarker to measure AVB-500’s success: serum levels of AXL versus GAS6.

Relying on this biomarker, Aravive shows a significant increase in mPFS for patients that meet the threshold for the AXL/GAS6 ratio and that have never taken Avastin.

With a similar increase in median overall survival.

As well as showing the combination of AVB-500 and PAC could see a higher response rate for patients that are not response to chemotherapy - having short platinum-free intervals.

This slide reinforces the previous slide with papers from 2013.

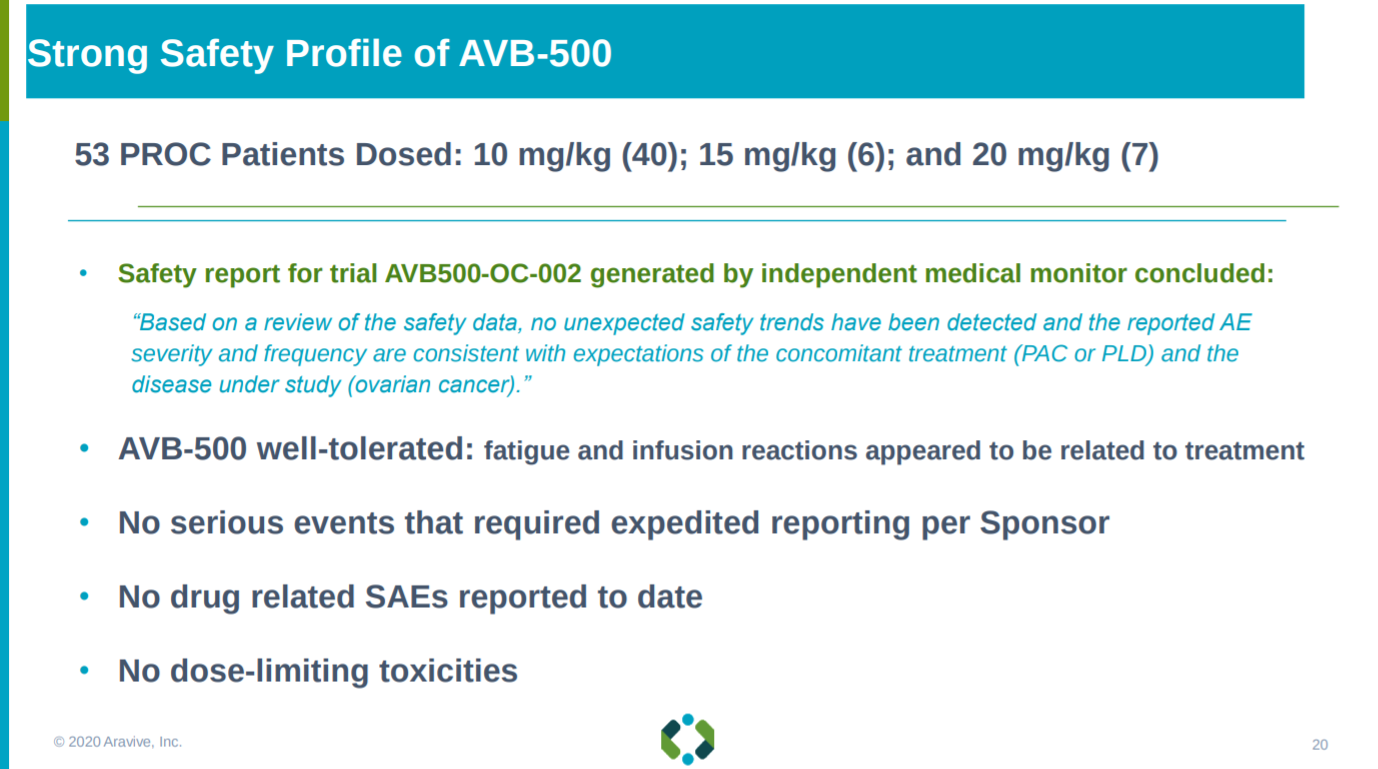

With efficacy signals from phase 1, this slide explains the safety profile of AVB-500 - no serious adverse events so far is pretty good.

Given this safety data, Aravive is going with the higher dose (15 mg/kg), which is always a great sign for their pivotal trial in PROC.

The next slide gives an overview of their phase 3 strategy: relying on their AXL/GAS6 biomarker and focusing on the AVB-500 and PAC combination.

With Aravive’s phase 3 trial design laid out.

Aravive goes into AVB-500’s advantage in PROC: (1) no safety concerns (2) strong, early ORR and mPFS signals (3) biologic with high affinity for GAS6 that should have minimal impact on normal tissue (4) AVB-500 doesn’t compete for metabolism with chemotherapies so synergies should be maintained in a larger trial (5) subverting targeting AXL directly, which can have off-target effects, and focusing on GAS6 to turn on AXL signalling.

Aravive also shows data of the AVB-500 and PAC combination in ovarian and peritoneal cancer.

With similar advantages as in PROC.

After ovarian cancer, Aravive is pursuing ccRCC.

Which has high expression levels of AXL.

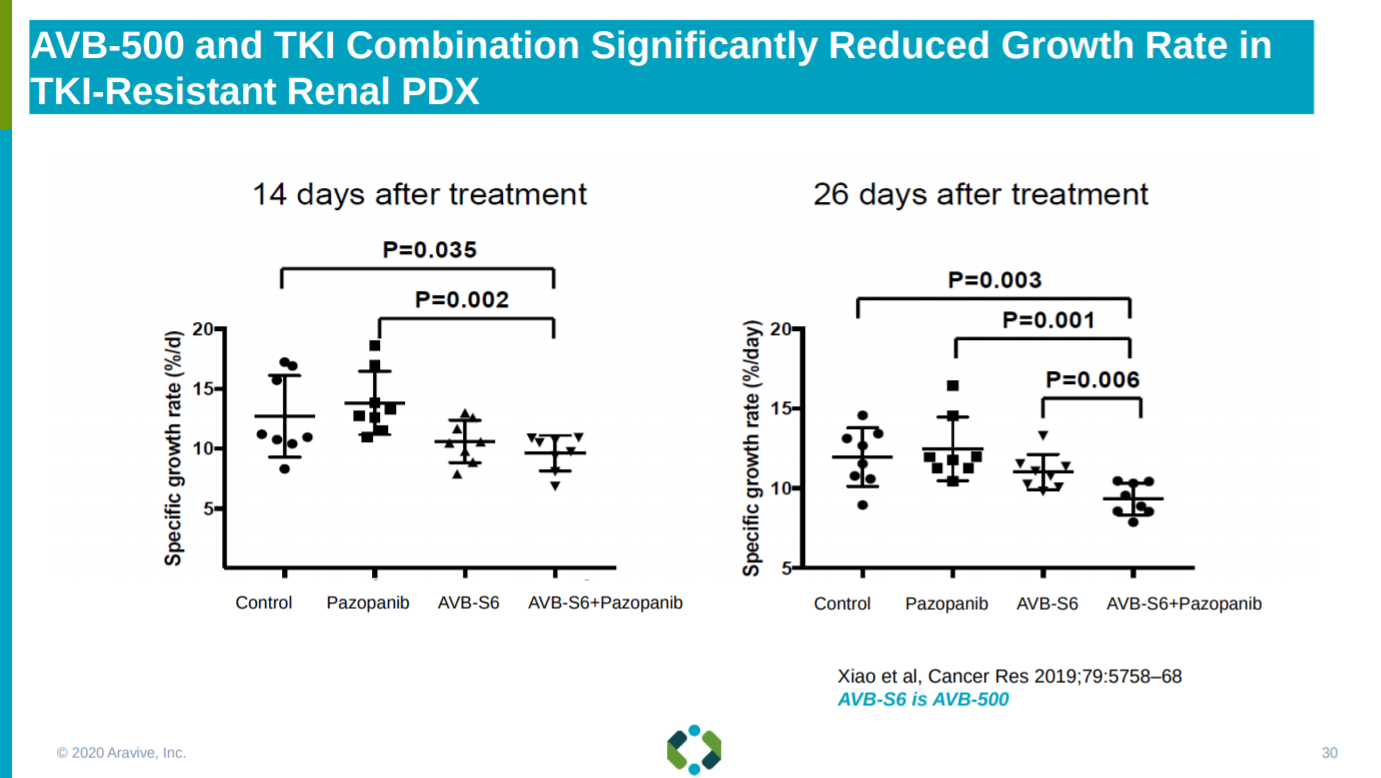

With data in mouse models showing efficacy of AVB-500.

With reduced renal cancer cell growth rates when combining AVB-500 with several tyrosine kinase inhibitors (TKI).

With the phase 1/2 trial design for AVB-500 in ccRCC explained.

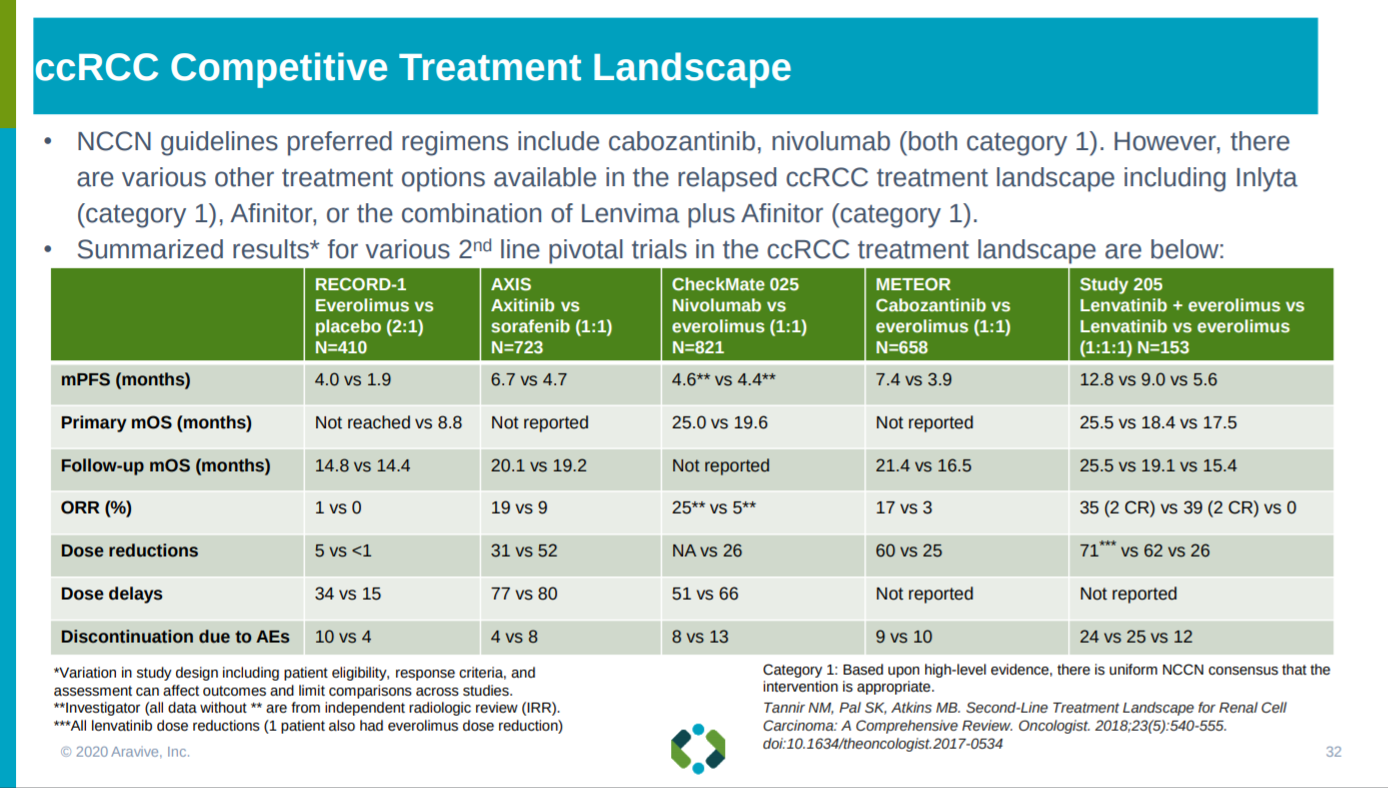

With the treatment comparables in ccRCC and the bar AVB-500 has to hit presented.

This slide gives an overview on the market opportunity for AVB-500 in the first two indications pursued: PROC and ccRCC.

With multiple large addressable markets for AVB-500, Aravive is looking to use basket trials to make this expansion more efficient.

The next slide goes into future trial designs for AVB-500 - basket trials to combine Aravive’s lead asset with PARP and PD-1 inhibitors.

For this combination strategy, Aravive goes into the market opportunity across a wide-set of solid tumors.

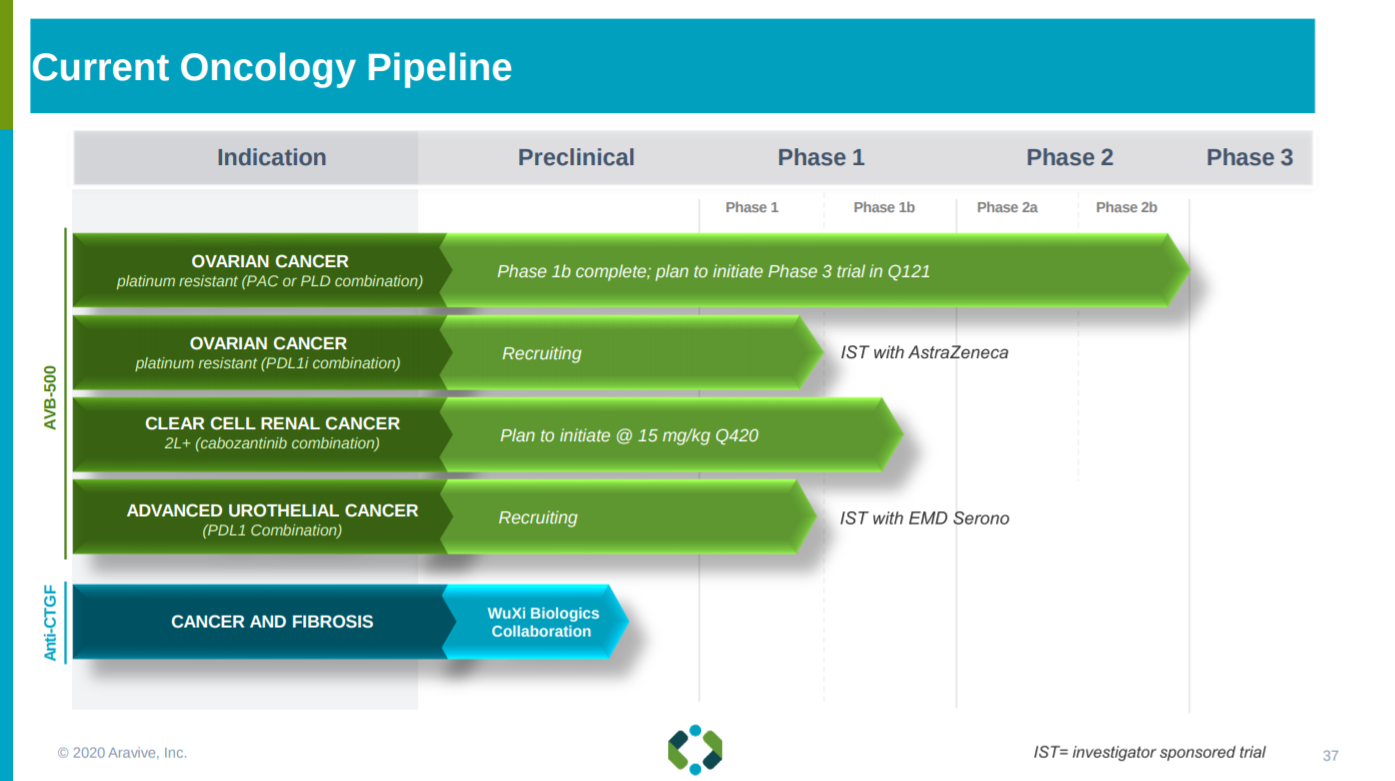

After characterizing its clinical strategy, Aravive ends this section with its pipeline - mainly AVB-500 and a bispecific antibody against CCN2.

The next slide goes into the antibody against CCN2 and the Collaboration with WuXi Biologics around the drug candidate.

Then Aravive goes into the MoA of CCN2, which is essential for growth of PDAC.

In series with the WuXi collaboration slides, Aravive explains their other collaboration with 3D Medicines to commercialize AVB-500 in China.

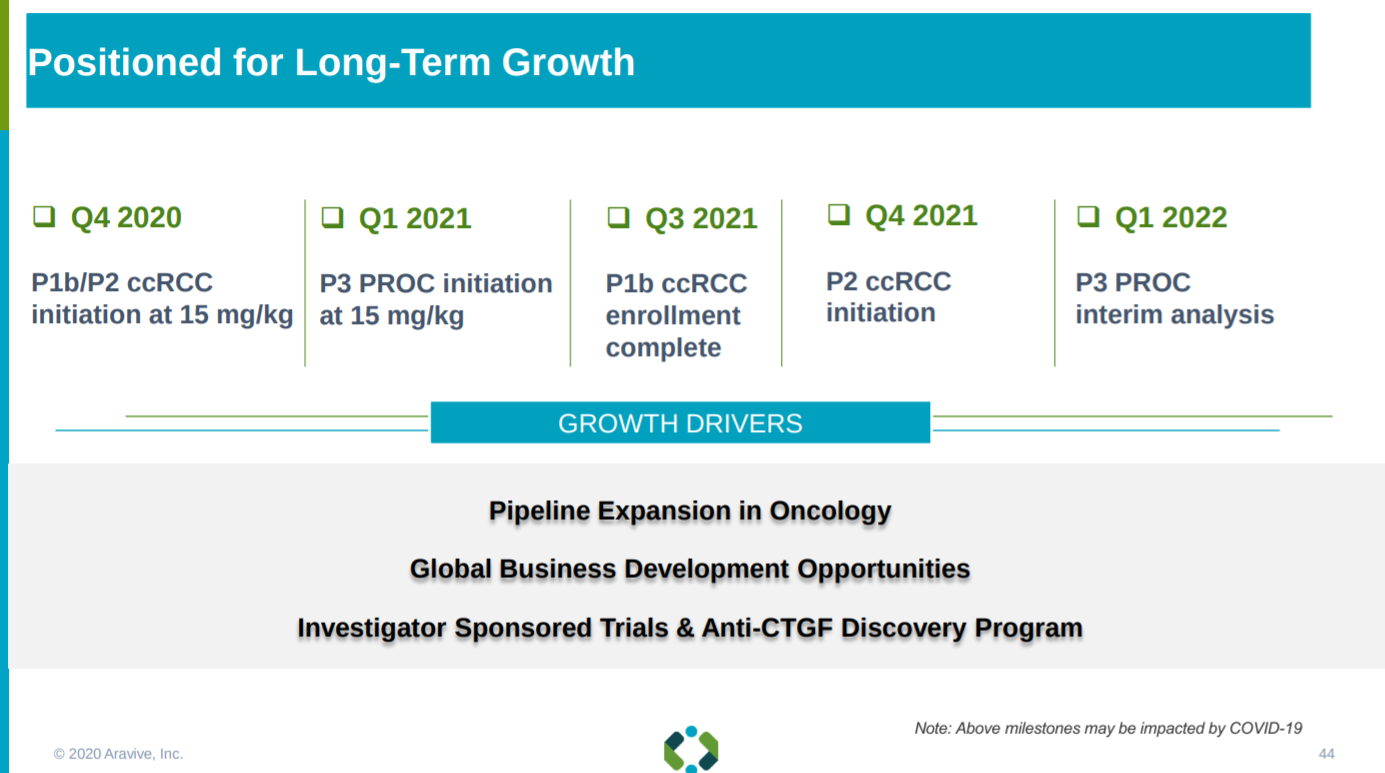

Near the end of the presentation, Aravive lays out their milestones and potential catalysts.

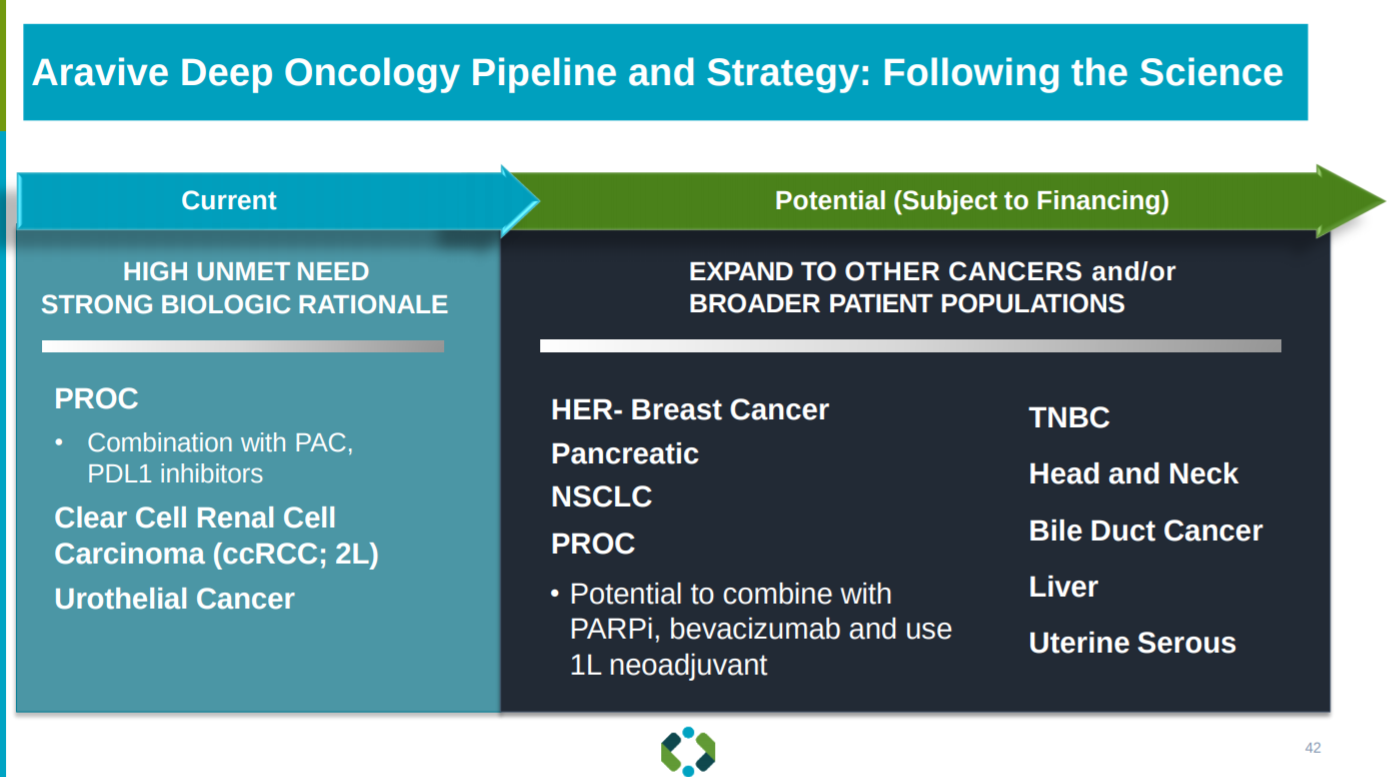

Aravive’s long-term strategy is to expand their lead asset to more solid tumor indications following the drug as a pipeline strategy.

This slide gives a brief overview of Aravive’s runway - they are going to need more cash to complete their pivotal trial. With a market capitalization under $100M, a little over half of Aravive’s value is its cash; they will need to partner up to generate sufficient capital to get AVB-500 closer to approval.

With this runway and implication of needing more capital, Aravive ends the presentation with their growth strategy: more clinical catalysts that opens up more partnership opportunities and hopefully a rising stock price.

Aravive’s presentation shows the potential of AVB-500 to treat multiple solid tumor indications. However, this potential is pulled back due to the capital constraints on the company. The upcoming pivotal trial of AVB-500 in PROC will be a major event over the next 2 years along with an expansion of their pipeline.

Follow up questions for the team:

What progress have been made for partnerships around AVB-500? With the goal to extend Aravive’s runway.

Any updates on the progress of AVB-500’s potential basket trial? This is a key part of the story to reduce the overall cost of the company’s future trials, especially with the capital constraints right now, and the long-term strategic goals of Aravive to pursue multiple solid tumor indications with the candidate.

How much will the phase 3 trial for AVB-500 and PAC in PROC cost? How will Aravive finance this work? Issue equity or another pathway?