Axial - Observations #16

Life sciences reflections

Build with Axial: https://axial22.axialvc.com/

Axial partners with great founders and inventors. We invest in early-stage life sciences companies such as Appia Bio, Seranova Bio, Delix Therapeutics, Simcha Therapeutics, among others often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you - email us at info@axialvc.com

Observations #16

A set of ideas and observations from a week’s worth of work analyzing businesses and technologies.

Remote trials and call centers

Remote trials need call centers. In 2011, Pfizer initiated a revolutionary, fully-remote clinical trial (REMOTE) to test the efficacy and safety of tolterodine tartrate treatment for patients with overactive bladder (OAB). The plan was to enroll 600 patients with only online tools. The trial was cancelled after only enrolling 18 patients. The key issue was that patients were uncomfortable putting their medical information through an online portal and were not provide enough guidance throughout the process:

From Pfizer themselves, the REMOTE trial can be broken down to a few components:

Online recruitment

Screening and consent

Remote drug shipment

Centralized investigator engagement

Remote patient monitoring for clinical trials

Mobile for self-reporting data

This workflow along with the value prop of a remote trial makes this seem very plausible to do for at least investigational orally-available drugs. From doing some reading on the REMOTE trial, it seems quite simply that patients just want some support along the way as they use web tools to try a new drug. Call centers seem like an easy way to solve this. I am not sure if companies like Five9 and Talkdesk could pull this off? Are there regulatory barriers like HIPAA - if so, that’s a large opportunity for a new company?

Standardizing small molecule discovery

There are a long list of licensing companies that have built large businesses handing off developable drug candidates to larger biopharma companies in mAbs (i.e. Adimab) and AAVs (i.e. Regenxbio). A similar business model in ASOs is probably next. Anyone building a company here? However, why is licensing of small molecules systematically not as large when compared to antibodies? DiCE Molecules tried but realized they need to validate their DEL technology clinically before giving enough confidence to more partners to want to license their chemical matter.

Small molecule discovery is still a messy process where drug developers throw the kitchen stink at a target to see what sticks. The issue is that the prior of any given small molecule is low because a set of reliable rules have not been developed to search small molecule space efficiently. Lipinski’s Rules exist but this framework was developed decades ago. ASOs and AAV have sequenced-based rules. Antibodies have predictable design processes. Small molecules kind of have a framework but they break down for subclasses.

What companies or labs have made enough progress to go from a small molecule design to screening (in vitro/vivo/silico) to an optimized molecule as reliable as antibody development? Atomwise is doing good work. Unnatural Products is building a predictable framework for natural products.

What can be done to accomplish this?:

Large-scale pairwise screening between libraries and targets to build out priors

Diverse scaffolds that are known to bind targets that can be used as drug screening starting points

Computationally pare down chemical space searched

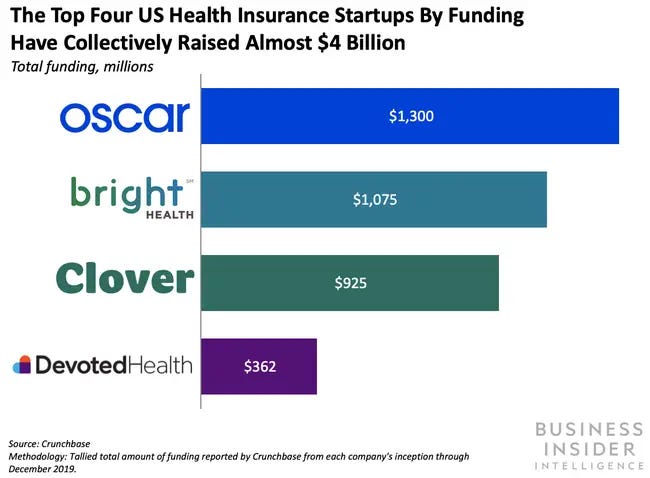

DTC Insurance

Direct-to-consumer (DTC) business models are very powerful: a business can access large populations with diverse buying habits. A drug company has two customers: biopharma and payors. Insurance companies, especially employer plans): employers and the government. Often in healthcare, individuals have little buying power.

Most things in life sciences flows from payors and insurance companies. So the recent development of large DTC health insurance companies like Oscar and Devoted Health has the potential to transform healthcare and drug development. So what are the opportunities/challenges:

Transition to fee-for-value. Incumbents rely on fee-for-service and have had troubles making the transition. This creates a massive opportunities for new entrants.

Owning the consumer relationship - traditional DTC, Medicare Advantage (MA) plans for individuals and families, and employers. Oscar is pure DTC, and Devoted among others is MA. Over the next decade - will employers give employees more ability to choose insurance plans as a hiring advantage.

High levels of customer service - treating healthcare as a concierge service (i.e. One Medical)

Scaling up consumer relationships and customer service with software: processing claims, identifying at-risk patients, fully integrating services, minimizing duplicative care, efficient scheduling.

Focused care providers or insurance plans. Companies like Virta Health could essentially become an insurance company themselves for their patient population - they have the patients, software capabilities, and customer service. Focused healthcare network could potentially be more profitable and effective.