Axial - New frontiers #3

Axial - New frontiers #3

New frontiers in life sciences

Axial partners with great founders and inventors. We invest in early-stage life sciences companies such as Appia Bio, Seranova Bio, Think Bioscience, among others often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you - email us at info@axialvc.com

New frontiers #3

ADCs

Cultured meats

Phenotypic screening

Industrial enzymes

Chemokines

Building the US-version of WuXi

Infectious disease

Immunometabolism

Fast following in drug development

Single-cell sequencing

As always, any list or group of companies is not comprehensive; some companies are stealth-mode and it’s not appropriate to discuss them publicly and I don’t like spending too much time copying and pasting logos.

ADCs

Antibody-drug conjugates (ADC) combine the specificity of an antibody and the killing activity of a conjugated cytotoxic agent. The 3 main components of an ADC are:

A monoclonal antibody - key features are minimal immunogenicity, high affinity for a cancer-specific antigen, stability for a longer half-life, and internalization to deliver the cytotoxic agent

A cytotoxic agent - usually targeting DNA or microtubules to initiate cell death; key features are to ensure that the molecule can be conjugated to the linker, is water soluble, and is stable. The main cytotoxic agents used are calicheamicins, auristatins, and maytansines.

A chemical linker - this is probably the most important part of an ADC and determines the drug’s PK/PD and stability; you have to make sure a linker only breaks in specific environments to avoid delivering the cytotoxic agent to healthy tissues. Linker’s come in 2 types: (1) cleavable depending on the environment to become activated and (2) non-cleavable that relies on lysosomal degradation of the antibody to release the agent. For example, Adcetris (Seattle Genetics) uses a cleavable linker sensitive to proteases while Kadcyla (Genentech) uses a non-cleavable one.

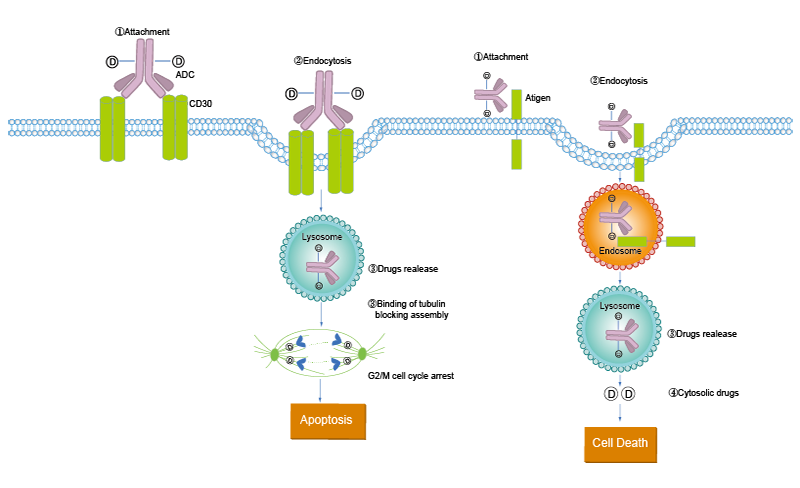

Once an ADC is designed, the drug modality kills a cancer cell through a series of steps that have to be accounted for during the design process:

The ADC binds an antigen through its antibody component

The ADC/antigen complex is brought into the cell through endocytosis

The linker is degraded. For ADCs with cleavable linkers, this step occurs within the endosome while in ADCs with non-cleavable linkers, the cytotoxic agent is released after protein degradation in the lysosome.

The cytotoxic agent is released

Apoptosis in the cell is initiated

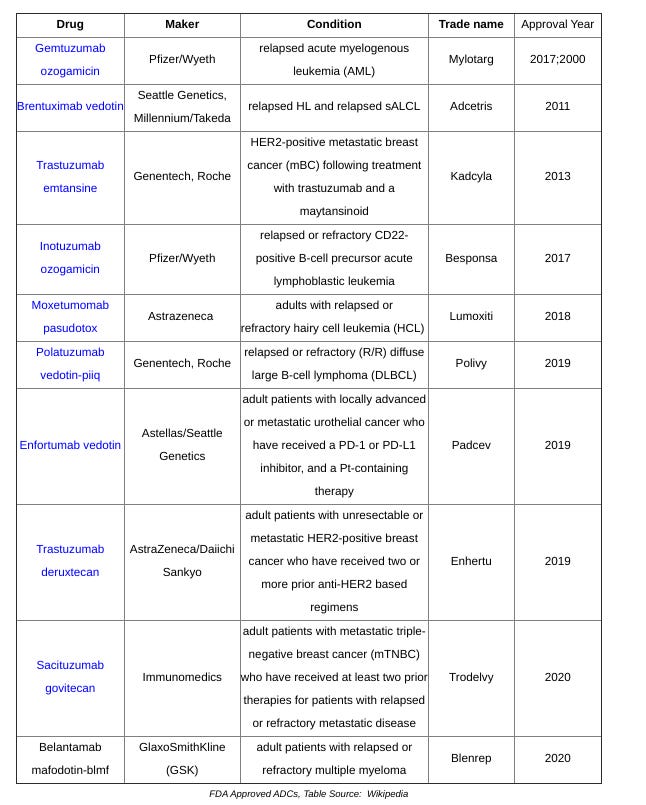

With 11 approved ADCs and over 80 trials ongoing, the field’s progress has seen a recent acceleration with 3 approvals in 2019, 2 in 2020, and 1 so far in 2021. The field has made a major comeback over the last 2 decades - companies have learned from past failures and have developed new linkers and chemistries to overcome the setbacks, mainly toxicity due to non-specific linkers, that many ADCs faced. Many of the new ADCs approved rely on the design of Seattle Genetics’ Adcetris, which was approved in 2011 for Hodgkin lymphoma and ALCL:

The 4 main problems ADCs have faced are:

Off-target effects mainly due to imprecise dosing

Low penetration into a tumor

Potency of cytotoxic agent

Stability problems that lead to shorter ADC half-lives

Another way to look at ADCs is as a systemic chemotherapy. With the specificity of an antibody, the selectivity of toxicity for cancer can be increased. The modality has always had promising data in model organisms that failed to translate into humans due to dosing problems. Developing better linkers can reduce off-target effects and expand the therapeutic window for an ADC when trials are initiated. The main levers for linker stability are matching the type (cleavable versus non) to the environment and picking the right site on the antibody for conjugation. For the latter, the traditional conjugation sites on lysine and cysteine groups, due to their nucleophiles; however, specific sites are being engineered into antibodies to generate homogenous populations of ADCs.

For penetration, specifically in solid tumors, an ADC has to be able to generate a lethal concentration of the cytotoxic agent in all cancer cells. If distribution is heterogeneous, then some tumor cells are more likely to develop resistance to the ADC. A useful strategy here is to conjugate helper proteins, such as tissue-penetrating peptides, to the antibody. This is where costs can go up significantly during the design process for an ADC. Picking the right cancer model and measuring penetration across each run is essential for success.

Moreover, an ADC’s drug-to-antibody ratio (DAR) combined with the cytotoxin itself determines potency. Increasing the ratio of cytotoxic agency attached to the antibody increases potency, but can lead to off-target effects if a linker is not specific enough. This is where the design process becomes important because balancing the relationship between a linker and DAR can make or break an ADC’s potential for approval.

Finally, a major consideration for ADC stability is managing the hydrophobicity of the cytotoxic agent, which can lead to ADC aggregation. Linker stability in blood is important to reduce off-target effects. Ultimately, the key to success for ADCs is designing the entire drug rather than focusing on optimizing for one component over another. New opportunities in the field are:

Inventing new linkers (mainly ones that react to new environments) and finding other ways to conjugate them to antibodies

Developing new penetrating agents to add to an ADC

Testing other cytotoxic agents

Implementing new stability moieties to the antibody

Cultured meats

Cultured meats bring technologies developed over the last few decades in cell culture to food production. In 2013, the Post Lab at Maastricht University developed the first cultured meat product - a beef hamburger patty that cost around $300,000. This work led to the founding of Mosa Meat and kickstarted the current boom in cultured meats. In the current backdrop of the success in plant-based meats and technological advancements that make that same hamburger made in 2013 cost $10-$20 to produce today, cultured meats have the opportunity to transform the trillion-dollar industry spanning beef and poultry to seafood and pork.

With a biopsy from an animal, the cells (often stem cells that can be differentiated into muscle, fat cells) are grown in a nutrient-rich environment. Most growth medium contains fetal bovine serum (FBS), which is derived from dead calf blood. On a side note, there is a need for serum-free media. During cultivation, more than 1 trillion cells (strands of muscle) are grown and can form complex structures depending on the scaffold and mechanical stress applied.

This technology can potentially have several large effects on the meat industry and environment:

Having an increased ability to optimize meat for higher nutrition

Produce meat with different resources - cells versus animals. This has the potential to reduce land/water use and reduce methane emissions. Although more research is needed to understand these effects because the land impact is not exactly clear and fossil-fuel powered meat incubators might have the same carbon dioxide footprint as factory farming.

Reduce food contamination from salmonella and E. coli and the use of antibiotics. However, there are risks of using excessive hormones during the cultivation process for cultured meats.

Reconfigure the supply chain of protein sources

Contribute to feeding a larger global population with a current limit on arable land

With the recent commercial success of plant-based, and fungi-based, products driven by Impossible Foods and Beyond Meat, cultured meat companies can build on top of this market growth and increase consumer adoption for alternative meats. Current plant-based products are easier to produce than the cultured equivalent but have some limitations on texture, sensory experience, and taste. There is a large opportunity to bring new tools in machine learning and synthetic biology to solve this problem for plant-based foods. Cultured meats can solve this problem too by creating completely new products or as a hybrid with plant-based foods to make those more realistic.

The key themes that will enable new product development and business growth in the field are (1) regulatory, (2) partnerships, and (3) consumer adoption. In 2018, the US Department of Agriculture (USDA) and the US Food and Drug Administration (FDA) announced a joint regulatory framework for cultured meat products - the FDA will regulate the early stages of product development (i.e. inspect culturing facilities) and the USDA will oversee the process closer to commercialization (i.e. product packaging, cell harvesting). Globally, India, the EU, Singapore among others have taken similar steps to provide clarity for companies. Partnerships are enabling new companies to gain distribution and institutional knowledge. Tyson investing in Memphis Meats is a great sign; however, more work needs to be done. Consumer adoption will be driven by cultured products having cost parity and similar texture/sensory/taste profiles as animal-derived meat.

Scaling production and new business models are 2 of the most important opportunities in cultured meats. Creating manufacturing processes that can produce 100Ks to millions of kg of meat at-or-near cost parity is essential for the field’s success. Moreover, moving beyond vertical integration for alternative foods in general has the potential to accelerate product development and create standards:

Building CDMOs that cultured meat companies can plug into and avoid implementing manufacturing themselves. Incumbents could easily move into this space but are currently hesitant due to the lower product margins versus drug development. This work has the potential to bring cultured meats to industrial scale.

Unlocking growth factors and standardizing growth media (along with bioreactors). Open source business models are an exciting solution to do this work. Another large opportunity is replacing FBS in large-scale production.

Cell line development with different growth features and biobanking requirements

New scaffolds to help cultured meats mimic the natural cuts from the fibers and connective tissue to blood vessels, nerves, and fat

New culturing techniques to include oxygen perfusion and micronutrient enhancement

If vertical integration is no longer a prerequisite, then cultured meat companies could license their products as meat products and ingredients

Phenotypic screening

Drug discovery as we know today really started off with natural products and finding chemical matter that leads to a biochemical change or a change in physical appearance. Phenotypic screening focuses on identifying phenotypes (and rescues) of interest. The power of genomics and structure-based drug design has revolutionized many parts of drug discovery by flipping this process to start at a particular target or pathway; however, phenotypic screening is still useful in some contexts where the underlying biology hasn’t been fully characterized. As a result, it is an old technology still useful for new problems. Moreover, this approach is not only useful in drug development. Phenotypic screening could bring transformative products in consumer products among other markets - Revela is leading the way here.

In 2015, a team at Pfizer published a paper defining the key rules for a phenotypic screen:

Selecting physiologically-relevant cell types and models. Examples are iPSCs, organoids, and even animal models. In vitro models offer higher throughput versus in vivo models that might have more accuracy. Parallel Bio is the leader here.

Designing assays the are relevant to a disease

Defining assay endpoints that are similar to clinical endpoints. This is focused on using biomarkers or disease signatures that are matched to clinical samples.

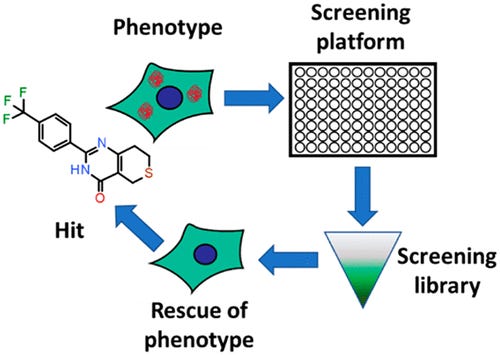

These types of screens can be divided into 2 major steps: (1) simple primary assay to cover as much chemical matter as possible and (2) complex, physiologically-relevant models to hone in on interesting hits. After the model is established, a large library of molecules are screened to measure something like expression changes in a panel of proteins or cellular characteristics like proliferation. Secondary assays are used mainly to counter screen and filter out molecules that have general effects. This is the part where phenotypic screening has higher upfront costs versus target-based programs. Automation of high throughput screening helps here as well as filtering hits more accurately with transcriptomics, proteomics, unsupervised machine learning, high-content imaging, and other tools within the assays themselves. Hits are then grouped into mechanism classes to prioritize them with a focus on target deconvolution. Even though many approved drugs have been approved without a known target, this knowledge is incredibly important to de-risk a program. Excitedly, this information is much more accessible with the wide-array of tools: panels of known target classes are screened against, activity-based protein profiling is very useful along with compound-immobilized beads, photoaffinity labeling, and cellular thermal shift assays.

In drug development programs, the key focus is formulating and testing a hypothesis. In target-based discovery, the process tests a hypothesis (biological, clinical, commercial) by generating a hit for a given target then going to lead selection and optimization and finally into pre-clinical/clinical testing. Whereas, phenotypic screening generates a hit for a given phenotype then the trick is to find the target. The latter process can get tricky sometimes and can make lead selection a bit more difficult, and as a result, better frameworks are needed to make phenotypic screening as structured as target-based programs:

In vitro models that are relevant for more diseases. Patient-derived cell lines are a step forward here, but could lead to unexpected variance in assay conditions. Co-culturing is also another useful approach but could impact throughput.

With more complex assay designs, identifying important variables that influence reproducibility and disease relevance.

“Chain of translatability,” an idea from biopharma, to connect assay endpoints to a clinical outcome.

What other tools are needed to advance phenotypic screening?:

Increasing the screening throughput of more complex models like organ-on-a-chip and organoids.

Translational work to build models for diseases that have recent breakthroughs in their mechanisms-of-action (MoA) and hopefully genetic drivers especially in CNS. On a side note, phenotypic screening is likely going to make a very large impact on longevity drug development.

More accessible proteomic tools particularly for activity-based profiling during the target deconvolution step. This would speed up the process and lower the barrier to entry to use phenotypic screening because this step is the last and sometimes hardest.

Simply, more case studies and work to merge phenotypic and target-based screening. The idea would be to create a database enabling a phenotypic match from a virtual screen one day.

Industrial enzymes

Enzymes are the workhorses of the cell and a core part of industrial biotechnology. The thesis is to collapse supply chains with biology. And enzymes are uniquely suited to do this. They catalyze important chemical reactions to produce new products from detergents to specialty chemicals. Overall, the field has undergone roughly 4 eras:

Enzymes from animal sources - early 1900s

Enzymes from microbial sources - mid 1900s

Enzymes from genetic engineering - 1980s to now (Novozymes has been dominant here)

Enzymes from software - now (Aperiam Bio leading the way)

The industrial enzyme market started taking off in the 1960s with what would become Novozymes starting work in the 1940s among other companies. In the 1980s, in the backdrop of the biotechnology revolution, companies like Genentech with Genencor (now part of DuPont), Novozymes, and Genex started using cloning and genetic engineering on bacterial/fungal strains to start producing enzymes with higher yields and new functions. Genencor in particular did great work to bring new enzymes to products like Tide and ethanol. The workhorse for this period of growth was the host, bacterial or fungal, and deep-tank, fed-batch aerobic fermentation. On this, there is a large opportunity to pick different hosts specific for a given problem. Colorado Biofactory is leading the way here.

With applications from food and plastics to energy and textiles, the addressable market for enzymes is in the $10Bs. The key theme for enzymes is replacing organic chemistry. Organic synthesis often leads to environmentally-harmful byproducts but have logical steps to produce a target molecule. Whereas enzymes are useful to produce a natural reaction/product but are not characterized well enough to significantly eat away at organic chemistry’s use. This creates an opportunity to go through the large search space of enzymes and the reactions they catalyze to map out specificity, catalytic rate, and activity. A database of millions of these enzymes along with these features could create the standard. This would enable logical steps to use enzymatic reactions to produce a target molecule.

Bringing more engineering principles to this field is an important driver. Synthetic biology and new tools can build large libraries of enzymes and screen for functional variants. The key themes here are:

Standardization of parts – makes screening and discovery reproducible and scalable

Coupling screening to the synthesis and assembly of DNA

Modularity of parts between multiple chassis

More predictable outcomes – as more data is collected through screens various combinations of components will be discovered to work together

These principles create a tight feedback loop between new models and biology experiments to make novel predictions. As more experiments are conducted, a company can build a large knowledge base of what experiments not to do and reduce the search space to valuable enzymes with new functionality.

Successful case studies like Novozymes, Solugen, and Genencor initially pursued low-hanging fruit and expanded their platform to solve larger-and-harder problems. BluumBio and Rubi Laboratories among others are emerging companies to keep an eye on. Broadly, applications for industrial enzymes span drug development, consumer products, and industrials. Software unlocking new enzymes through better genomics analysis (finding new biosynthetic clusters) and design can discover enzymes that catalyze difficult chemistries (i.e. C-C) and expand the toolkit to help patients and our environment.

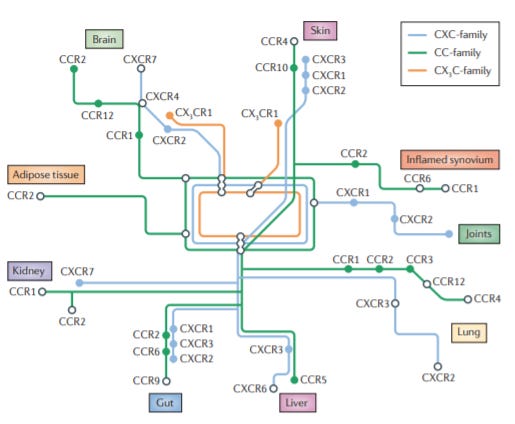

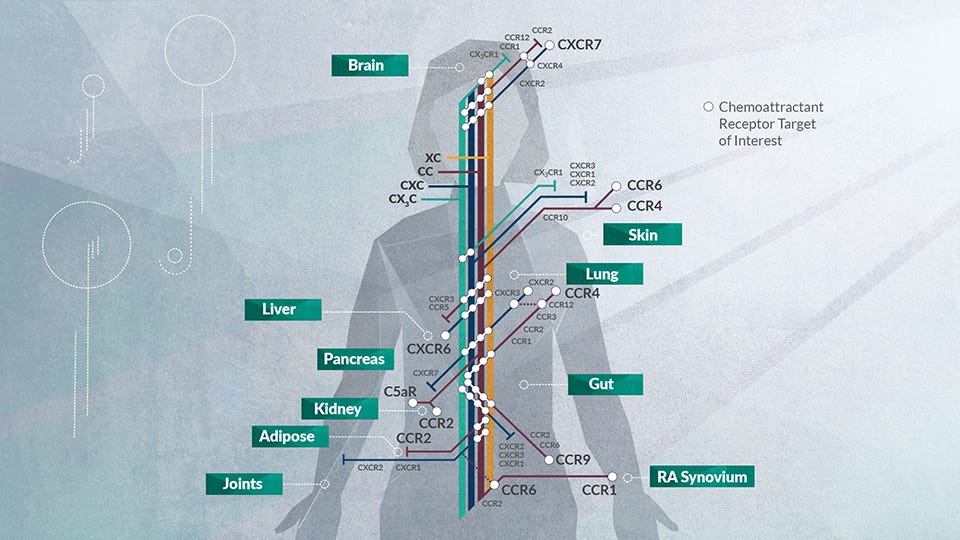

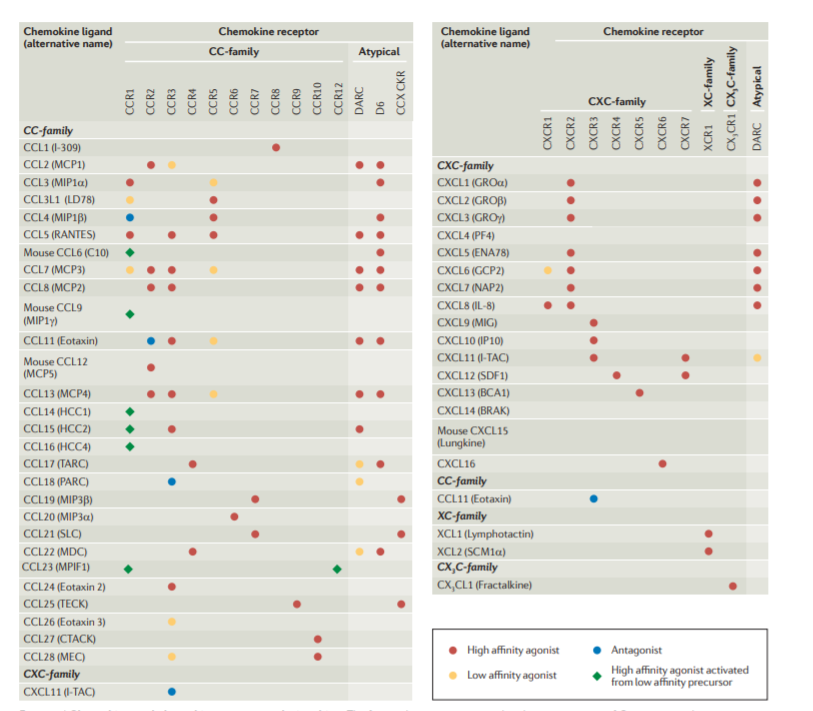

Chemokines

Chemokines are the trafficking control system for the human immune system. They act as signposts to get different immune cells into certain organs. With over 50 different chemokines and 20 receptors (which are GPCRs), they are a class of cytokines that induce chemotaxis in nearby cells.

In 1987, the first chemokine, CXCL8 (IL-8), was cloned for work around figuring out which factor(s) monocytes were secreting to attract neutrophils: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4459227/ & https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4456961/

This sparked large-scale research efforts to clone chemokines and their receptors in the late-1980s and 1990s. This work led to the approval of drugs targeting CXCR4 and CCR5 to treat HIV and C5aR for ANCA-Associated Vasculitis (AAV). Despite the large number of new drug targets for inflammatory diseases generated from this work, dosing and target selection have been barriers for more successful chemokine-focused medicines.

As a result, there is a large opportunity to develop new medicines that target the chemoattractant system: (1) small molecules, as well as antibodies, to selectively target chemokines and their receptors and (2) engineered chemokines:

For autoimmunity, chemokines direct immune cells to self tissue

Viruses and microbes use chemokines to deceive the immune system

Vaccine responses can be improved with chemokines

Chemokines drive inflammatory diseases like AAV, diabetic nephropathy (DN), inflammatory bowel disease (IBD; targeting CCR9), and rheumatoid arthritis (RA; CCR1)

In cancer, angiogenesis is influenced by chemokines

Other diseases like Type 2 diabetes (T2D; CCR2) and chronic kidney disease (CKD) have also been found to be driven by inflammation where chemokines play a major role

The complex orchestration of chemokines and their various interactions with receptors make this space hard-to-drug. Not only does the target matter but the location and time of intervention are important as well. New opportunities with chemokines are centered around target selection for a disease, chemistry, and in vivo

dosing:

Mapping in vivo interactions - figuring out systematically which chemokines bind specific receptors and at what doses and locations

Determining the biological response for each chemokine/receptor pair - different chemokines and receptors can have multiple functions depending on tissue, timing, and pairing. Excitedly, a small set of cells with activated chemokine receptors can lead to a large-scale immune response.

Immune cell subsets - which immune cell subsets respond to individual chemokines? For example in monocytes, CCR2 is a marker for an inflammatory class and CX3CR1 is one for the resident subset of monocytes.

Dosing - figuring out dosing in vivo; most work has been in vitro. Moreover, to generate a therapeutic effect, a large proportion of chemokine receptors need to be inhibited continuously, increasing the required critical dose. This requirement can lead to ADMET issues.

Target selection - determining whether a chemokine is redundant or not for a specific disease. For example, CCR7 is activated by both CCL21 and CCL19. But CCL5 also CCL5 activates 3 chemokine receptors: CCR1/3/5. Moreover, receptor internalization is different for each interaction. Chemokines have been seen as a hard-to-drug class of targets due to this potential redundancy.

Antibodies and engineered chemokines - develop antibodies for specific chemokines or receptors. Targeting chemokines, and using chemokines as a drug, requires knowing the concentration of the ligands in vivo. Also, drugging the receptors can become complex since they are GPCRs and have multiple transmembrane regions.

Ultimately, there is a large opportunity to bring new chemokine medicines to patients. The low-hanging fruit is to develop models and tools to predict which chemokine/receptor pair is involved in disease and develop a drug candidate to target the pair. In short, new methods are needed to figure out which part of the control system to block or add to?

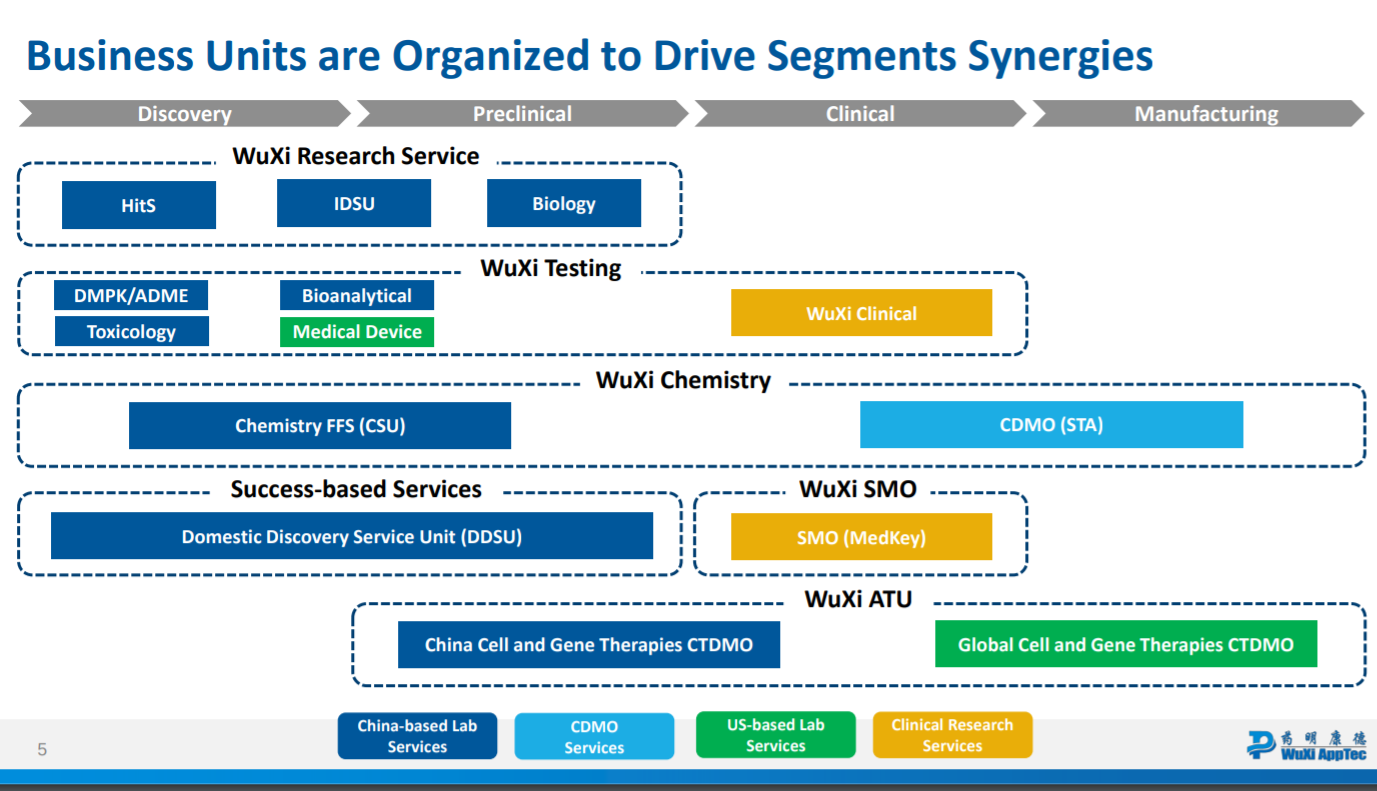

Building the US-version of WuXi

Driven by the theme of onshoring biomanufacturing, it is imperative that a US-version of WuXi is built. Resilience has a shot, but so many more companies need to emerge to take advantage of the opportunity and reinvent the CRO. WuXi was founded by Ge Li in 2000 as a services company for synthetic chemistry. Each and every year the company rolled out a new offering: manufacturing, bioanalysis, formulation, AMDET. Charles Rivers Laboratories had the opportunity to buy WuXi in 2010 but ended up nixing the deal. Over the following decade, WuXi grew into one of the largest and most innovative contract-research organizations (CRO) in the world and positioned itself to dominate discovery services globally.

WuXi has been able to win for 6 key reasons:

Labor arbitrage - being in China gives WuXi access to a large amount of talent at much lower wages

Scale - Wuxi has a suite of services done at a large-scale built over 2 decades. The company offers services for a wide range of modalities from small molecules to biologics and cell/gene therapies. They provide discovery, development, and manufacturing services and even offer things like medical device testing and genomics products.

Flexible deal structures - WuXi has been flexible in the terms it provides to its customers. The company offers fee-for-service contracts with various milestones and royalties on some of the products if appropriate. Beyond services, WuXi is also aggressive with joint ventures and investing.

Founder-led company - Ge Li still runs the company and is motivated to complete his vision

Regulation - if a company outside of China wants to bring a drug, especially biologics, to China, they must meet regulatory requirements by repeating the development and manufacturing process in China again. This is a lucrative business for WuXi.

Standardization - WuXi gets lock-in by getting customers early and fully-integrating from discovery to manufacturing

These 6 drivers enabled WuXi to dominate services from discovery to development and finally to manufacturing. Now WuXi has set its sights on internal product development. The first example of this was WuXi spinning off its biologics manufacturing business into WuXi Biologics in 2015. This gives a glimpse into the future for WuXi in cell and gene therapies and beyond. WuXi Biologics focuses on fully integrating services for biologics drug development: (1) drug discovery, (2), pre-clinical work, (3) phase 1/2 clinical development, (4) services for pivotal studies, (5) commercial manufacturing. This end-to-end platform allows any customer to plug into WuXi but more importantly makes biologics development a lot more accessible. For WuXi Biologics, it’s probably more valuable that they get companies as early as possible because they will spend increasingly higher amounts as the research and trials progresses. Because WuXi Biologics is such an essential component for smaller companies with less resources and to larger ones that want access to the Chinese market, the company has been able to get royalties on some of the products produced from their services and are set up to build an internal pipeline.

It seems obvious that WuXi has the potential to take control of the global CRO market. With such a dominant position, there is a need to build a US-version. The end-state is easy to comprehend - it’s WuXi. But what are good first moves?:

Focusing on higher value products like cell and gene therapies

Building technology-enabled services that can take on WuXi’s labor advantages

Rolling up services to become fully-integrated at least for a region or specific area then expanding

Infectious disease

New medicines and vaccines for infectious diseases are always needed but the business of infectious disease has not been historically rewarded over the last few decades. Events like the COVID-19 pandemic reinforce the need for more sustainable businesses in the field - multidrug bacteria resistance, neglected tropical diseases (NTD), and communicable diseases in developing nations hopefully are given more attention and capital over the next few years.

However, building a business to develop new antibiotics and other infectious disease drugs are not currently rewarded. Starting a business to prepare for pandemics was not highly valued until COVID-19 hit. Finally, global public health is required to save more lives and a prerequisite for economic growth, but most companies do not currently have a global health mandate. To explore the potential of building a large business in infectious disease, it is worth profiling a few case studies who have had success in the field: Gilead, Moderna, Vir, Regeneron, AbCellera, Distributed Bio, Novavax, and BioNTech.

Gilead was founded in 1987 by Michael Riordan to cure viral diseases. Riordan had spent time in East Asia on a Luce scholarship after college. While abroad, he worked at a malnutrition clinic and came down with dengue fever. The exposure to another country’s healthcare system and experiencing the lack of medicine for viral disease inspired Riordan to go to medical school at Johns Hopkins and business school at Harvard to learn more about the business of medicine.

After working as a VC for a ~year, Riordan started Oligogen to use antisense DNA, an emerging technology in the 1980s, to selectively target viruses. The company’s name changed to Gilead after the Balm of Gilead, a medicinal product historically used in the Middle East. Riordan set Gilead on an ambitious path to cure viral disease and did everything to build a great team to accomplish this vision even persistently working to get Warren Buffett involved - https://www.scribd.com/doc/208120113/Michael-L-Riordan-the-Founder-and-CEO-of-Gilead-Sciences-and-Warren-E-Buffett-Berkshire-Hathaway-Chairman-Correspondence

The company was founded in the 1980s in the backdrop of the HIV epidemic. The same year Gilead was founded, 1987, AZT had just been approved by the FDA to treat AIDS patients. This created an urgency for Gilead and other infectious disease companies to develop new medicines for HIV/AIDS patients. Gilead’s timing was likely a major driver for its success - the need to develop new viral drugs was more acute than ever.

Early on, Gilead executed a deal with Glaxo for $8M to use their antisense technology in cancer. This enabled the company to have the capital to expand the purview of their platform: the most important part of this work was funding Antonin Holy’s lab. This led to Gilead’s first FDA-approved medicine in 1996 - Vistide for cytomegalovirus (CMV) retinitis in AIDS patients. Gilead continued to churn out new approved drugs, like Truvada for HIV infection, mainly from the golden goose they had in the Holy Lab. This work helped make HIV/AIDS a manageable disease for most patients.

In 2011, Gilead acquired Pharmasset for ~$11B. This acquisition gave Gilead the rights to two transformative medicines in Hepatitis C: Sovaldi and Harvoni, which ultimately cured the disease. Moreover, this event probably was the keystone moment for the significant growth of the biotechnology industry in terms of capital deployed and returned over the last decade. The size of the acquisition was one that hadn’t been seen since the early 2000s.

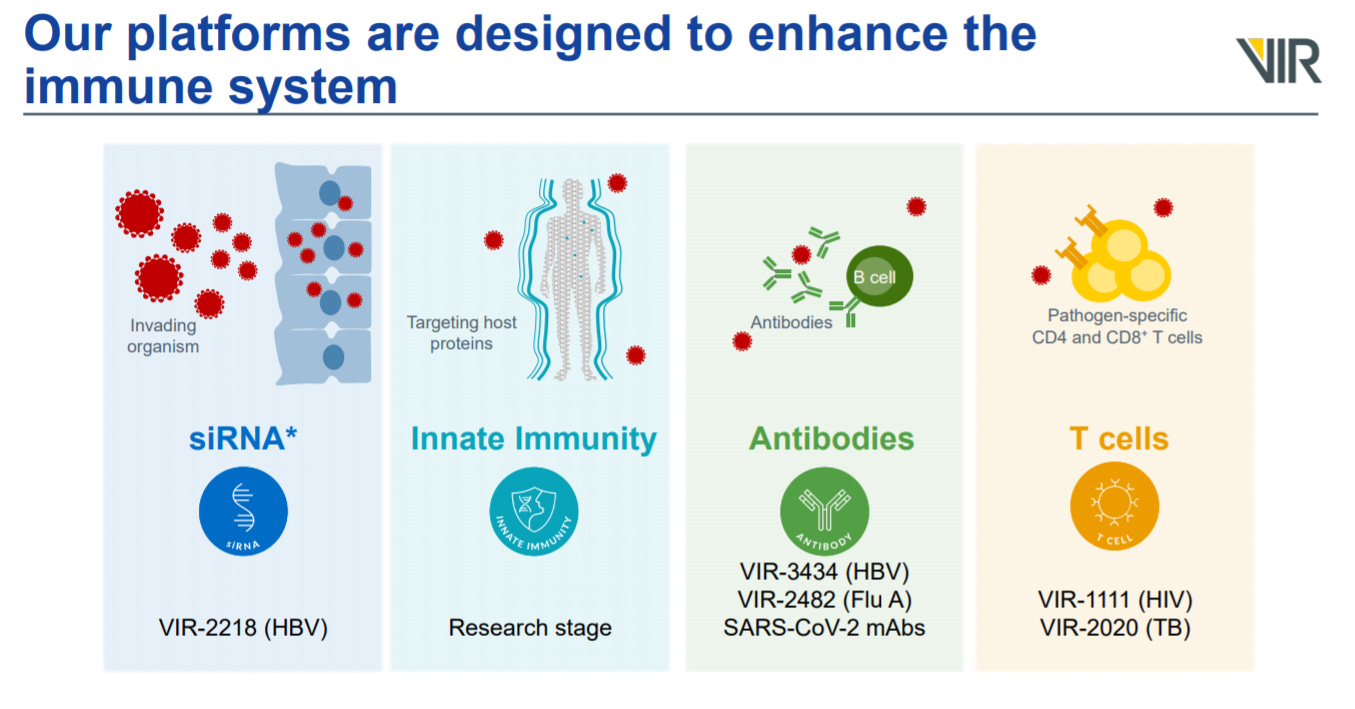

Another infectious disease company is Vir Biotechnology. Founded in 2016, Vir assembled an all-star team to program the human immune system to fight infectious disease. The business model was very broad - developing multiple modalities from antibodies to siRNAs, and in-licensing assets, building an internal pipeline, and funding academic labs. The company is still relatively early especially when compared to Gilead. But Vir has played a role in the response to the COVID-19 pandemic. What makes Vir unique is its focus on the immune system rather than a particular pathogen.

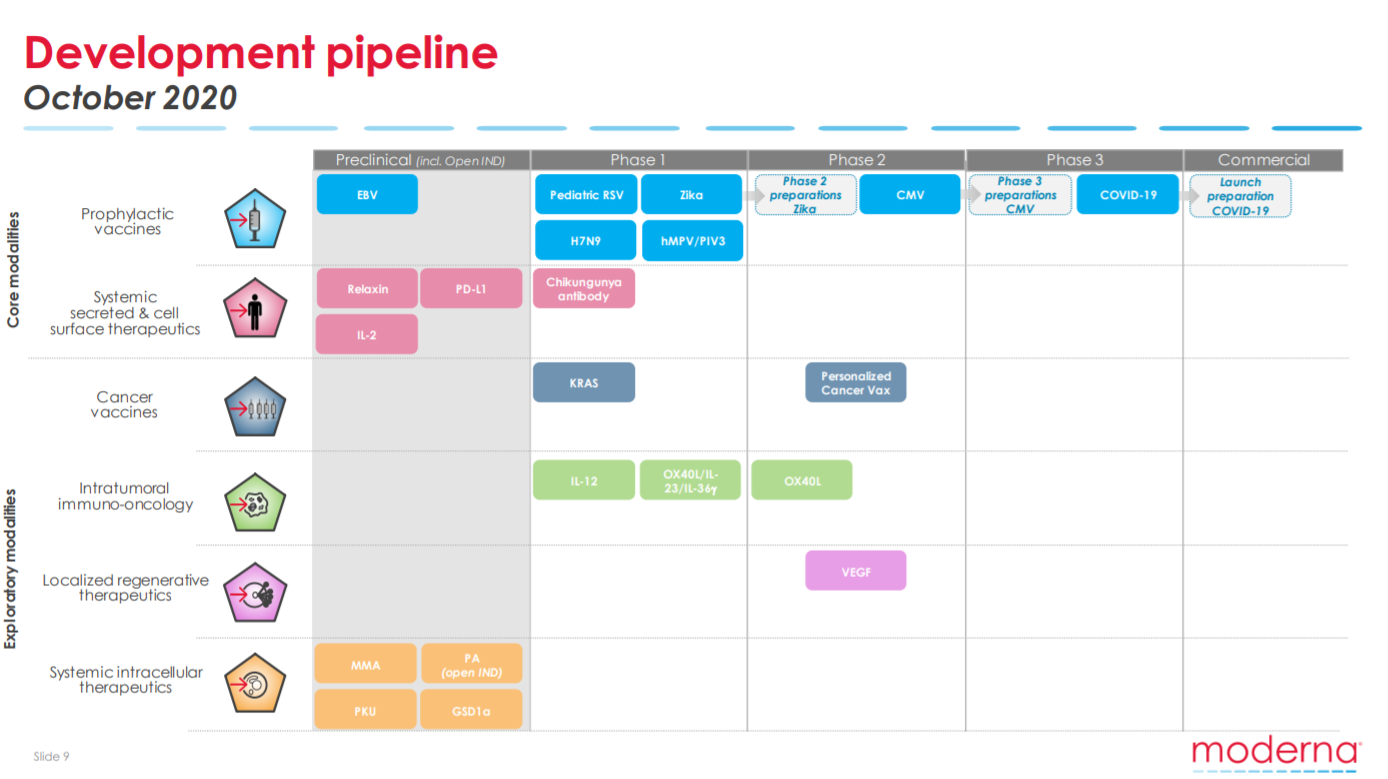

Moderna has played an essential role during this pandemic. Their recent vaccine approval, along with BioNTech/Pfizer, is a major breakthrough for patients and society. It also validates their strategy to use mRNA drugs as a platform for infectious disease and beyond. The modality has had a lot of promise over the last 7-8 years, but COVID-19 accelerated what would have taken ~5 years to a few months. With the right timing and business model, Moderna is set up to bring mRNA medicines to a wider set of patients over the next few decades.

BioNTech is very similar to Moderna. With similar technology, BioNTech is also positioned to bring mRNA medicines to more patients. However, the company is also ingesting other modalities, similar to Vir, into its platform.

Novavax has been around for a long time. The company was founded in 1987 (same year as Gilead) to develop vaccines for infectious diseases. With no approved medicines over its lifespan, Novavax has relied on its platform and funding from foundations and public institutions (i.e. BARDA and Bill & Melinda Gates Foundation) to stay alive. The platform is centered around a set of recombinant nanoparticles and their Matrix-M adjuvant technology with the goal to generate strong patient immune responses to a vaccine. However, the Moderna/BioNTech vaccine data in COVID-19 might make this work somewhat irrelevant for this pandemic. But Novavax has vaccines in development respiratory syncytial virus (RSV), seasonal influenza, pandemic influenza (H1N1, H5N1), Ebola virus, among others. There might be an opportunity for them to update the COVID-19 vaccine every 2-3 years depending on the evolving strains.

Other businesses like Regeneron, AbCellera, and Distributed Bio (now part of CRL) are focused on developing antibodies. They have more flexible business models where they license out assets in other disease areas and have the resources to invest in their underlying technology. This flexibility has enabled all 3 companies to rapidly respond to the COVID-19 pandemic.

Beyond drug development, curing infectious diseases requires a substantial role from public health. Everyone needs access to clean water and better nutrition. Maternal/reproductive health plays an important role. How do we increase accountability and prevent people from making decisions about other people’s health without consequences? Public health, things like vaccinations, trash pickup, sewage, and more, has a large impact on economic growth, lifespan, and wellbeing - https://oecdobserver.org/news/archivestory.php/aid/1241/Health_and_the_economy:_A_vital_relationship_.html:

“The effects of health on development are clear. Countries with weak health and education conditions find it harder to achieve sustained growth. Indeed, economic evidence confirms that a 10% improvement in life expectancy at birth is associated with a rise in economic growth of some 0.3–0.4 percentage points a year.

Disease hinders institutional performance too. Lower life expectancy discourages adult training and damages productivity. Similarly, the emergence of deadly communicable diseases has become an obstacle for the development of sectors like the tourism industry, on which so many countries rely.”

Can a sustainable and large infectious disease business be built without substantial government backing? Or is government backing a prerequisite? It sure seems so from the case studies. How can life sciences companies integrate with public health mandates? Can we set up a reward system to incentivize entrepreneurs and companies to eradicate diseases like malaria? Can we do the same for the deployment of rapid infectious disease diagnostics? What areas are just intractable and the realm of nonprofits? Can a universal vaccine be developed?

Key lessons:

Timing has been important. The HIV/AIDS epidemic helped kickstart Gilead and Novavax. The COVID-19 pandemic has done the same for BioNTech and Moderna.

Platforms are essential to also work on other diseases like cardiovascular and cancer. This enables a company to raise capital to invest in technology and have the capabilities to work on infectious diseases. During most eras, capital has not been available to standalone infectious disease companies. Vir was an exception mainly due to the team.

There is an advantage to being centered around human immunology instead of pathogen focused. Moderna and BioNTech validate this with their COVID-19 vaccine. This enables a more rapid response and a broader scope. Inflammatix is leading the way here on the diagnostics side.

There is an opportunity to connect drug development with a public health initiative. Beyond COVID-19, other opportunities are in NTDs and malaria.

Each case study, with the exception of Novavax, executed some form of the Merck model: focus on higher-value indications to subsidize programs with societal impact. In 1987, Merck freely distributed their medicine for river blindness. This was only possible because Merck had gotten Mevacor approved as the first statin the same year.

Immunometabolism

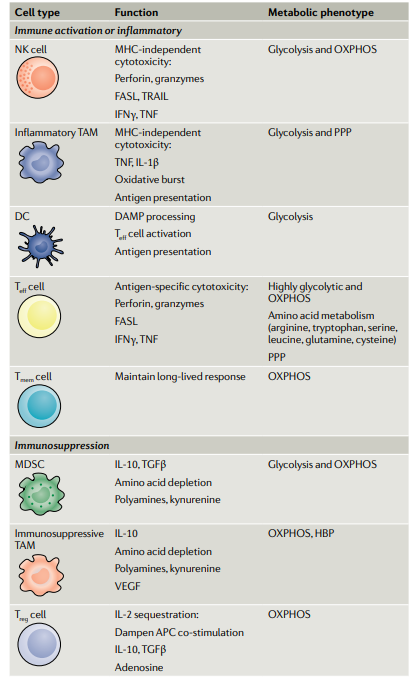

Metabolism creates a set of diverse tumor microenvironments (TME) across cancers and patients. Importantly, metabolism within each TME has a significant effect on immune cell function and the ability for immunotherapies and cell therapies to treat solid tumors. Particularly, immune and cancer cells actually converge on their metabolic pathways competing for the same resources to grow. This creates an environment to inhibit immune cells in the TME but also an opportunity to target metabolism to help immune cells kill cancer cells.

Companies like Agios (targeting IDH; although they recently sold off their immunometabolism portfolio to focus on PKA) have been built on the premise of targeting metabolism to treat cancer. However, the full potential of the field is still to be realized mainly due to the diversity of immune cells within the TME and the unique role of oxidative phosphorylation and glycolysis along with other pathways within immunometabolism.

Immunometabolism is such a complex field. Immunology is already hard enough. Adding metabolism on top of it only makes figuring out cause/effect relationships even more difficult. Opportunities in the field are:

Measuring the metabolism difference between a given tumor and immune cells in the TME

Assessing the metabolic requirements for each immune effector cell

Using this information to find weak spots in metabolism to pursue and develop new medicines. The hard part here is the differences might be so slight that therapeutic windows could be very narrow.

Fast following in drug development

There is a large opportunity to develop new business models to be a fast follower in drug development. Many branded drugs often have consistent price increases (>10% annually) over the lifetime of their patent exclusivity without any underlying improvements. This creates a market opportunity for other companies to fast follow on the branded drug and undercut on price by up to ~50%. Many biotechnology companies in China and EQRx are leading the way. EQRx recently reported data on an anti-PD-L1 antibody they licensed from CStone in China - this program serves as a proof of concept for the business model. The idea is to bring a Southwest Airlines or Danaher business model to drug development. Companies in China have been able to do this at least in their home country mainly due to labor advantages, larger patient populations, and streamlined regulatory processes. EQRx boldly got started to do something similar in the US and do fast-following more systematically.

To successfully have a shot at building an enduring business around a fast follower model a few things are needed:

Having an ability to design or discover patent-breaking drugs

Also, having the ability to execute more efficient clinical trials. A fast follower has to get to market before the branded drug goes generic. This probably means that the company has to initiate a program before a branded drug is actually approved. A company has to build forecasting tools to not only predict the success of their own drug but the success of the branded drug in trials.

Pursuing only established targets and mechanisms, which hopefully lead to lower clinical failures for the fast follower. This is also enabled by the increasing power of genomics over the last 2-3 decades; target discovery has been mostly commoditized.

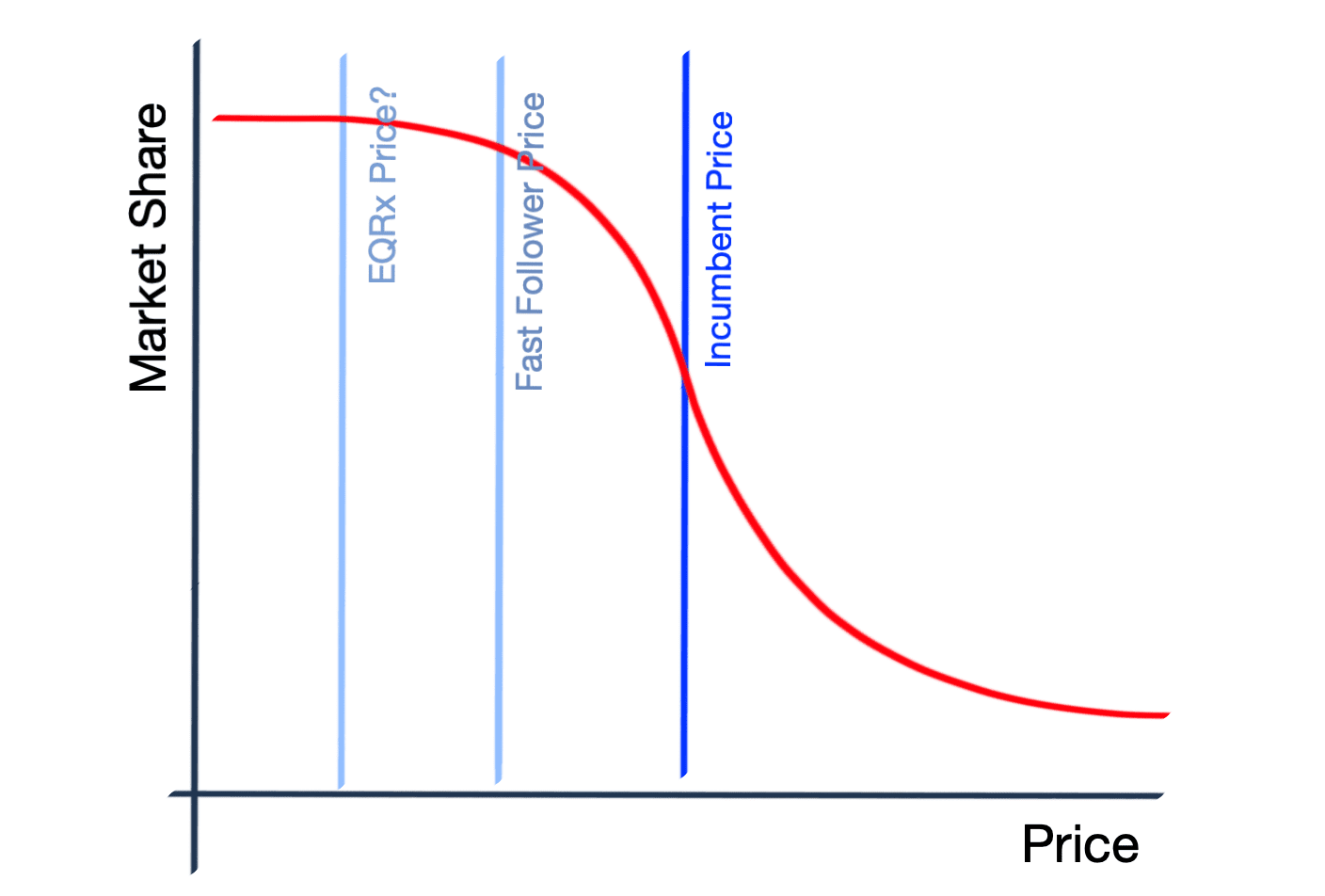

Identifying markets where the fast follower model can expand the market or get a higher share (figure below from EQRx). If the fast follower is charging lower prices, there is a possibility that more patients, and their plans, can afford it. Other elements like competition, reimbursement, and market uptake are important here.

Establishing strong payor relationships to ensure patient access and quick market uptake

Ultimately, this model has the potential to commoditize some parts of drug development. For diseases with established targets and mechanisms, a company could build moats around commercialization, capital structure, and forecasting rather than discovery. This model is fraught with risks. Clinical trials are probably going to fail - is a company capitalized well enough to weather this? Executing faster trials is still hard even for validated targets. Patent issues can arise from this model. Incumbents will fight back - biopharma will use vouchers to shift who pays their high prices, a PBM could exclude the fast follower from their formulary, and more.

Source: EQRx

The fast follower also has the potential to be one of the first drug companies to actually delight their customers. So who could they be?:

Patients - building a brand around lower pricing and increased access

Drug companies - a source of licensing opportunities for the fast follower. A straightforward strategy is to bring assets from China to the US.

Payors - probably the most important relationship to help the fast follower lock in purchases of their drug and market access

Networks - hospitals in particular help the fast follower more easily recruit patients and run more efficient clinical trials. The new CMS rule enacted in 2021 on price transparency also helps the fast follower - https://www.cms.gov/hospital-price-transparency

Physicians - facing off against the large sales forces of incumbents, fast followers need to show non-inferiority and get payor help here

PBMs - with recent consolidation of pharmacy benefit managers (PBM), a fast follower could try to find a way to reward them or bypass them completely. PBMs are probably the stakeholder to focus on the least.

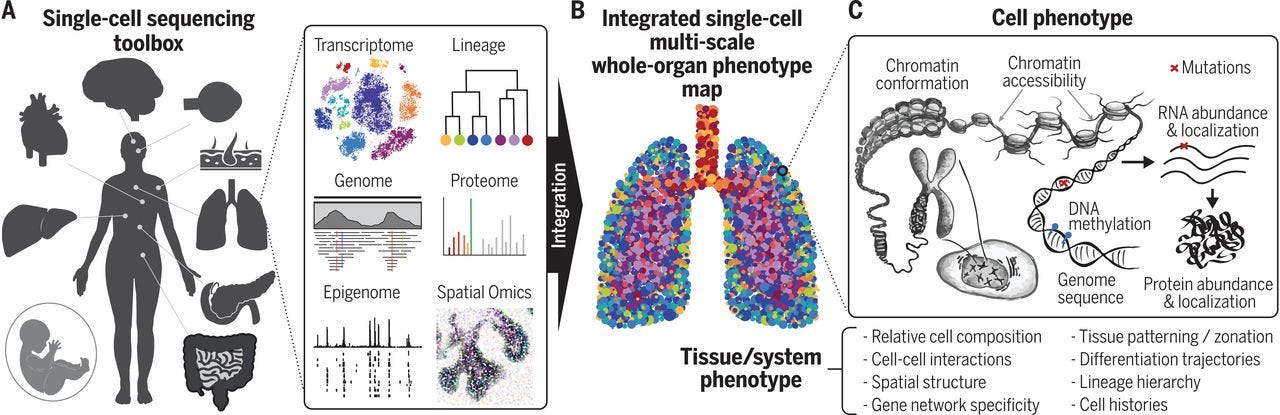

Single-cell sequencing

Single-cell sequencing, led by tools developed by 10X Genomics and Akoya Biosciences, are enabling many new avenues in research and applications in drug development and diagnostics. Up to millions of cells can be manipulated and profiled to measure their heterogeneity and individual gene expression. The human genome has around 30K genes that produce over 100K mRNAs (splicing creates more variants). Each cell expresses around 10K genes with a few thousand having cell-specific patterns.

In 2003, the Human Genome Project was completed enabling new applications in particular genome-wide association studies (GWAS). The goal of this work was to build a database of genetic variants and link them to different phenotypes and disease. Due to the underlying complexity of biology, GWAS never fulfilled the promise of genomics. Large-scale sequencing efforts driven by the super-exponential decrease in costs and Illumina, helped increase access to data and scale up this work. The next step has been sequencing single cells to understand cell-to-cell variation, not just human-to-human, and their genomes, epigenomes, transcriptomes and proteomes. New tools are needed.

Beyond single-cell sequencing, we are also moving toward perturbing biological systems to measure changes within them. A catalog of genetic parts are being discovered, which is setting up for large-scale perturbation studies of single-cells. Coral Genomics is a leader here. This work could finally fulfill the original vision of the Human Genome Project: linking genetic variants to different traits and diseases.

What are some of the important problems to solve in single-cell sequencing?:

Integrate new single-cell measurements and standardizing them between samples: DNA, RNA, proteins, methylation, chromatin accessibility, spatial arrangement

Increasing sorting throughput/efficiency in single-cell sequencing. This would lead to large gains in resolution and the number of cells profiled. In some situations, due to these limitations only a few 100 cells can be measured. This would increase the number of cell types we discover along with their developmental trajectories.

Better analysis and visualization tools to analyze higher dimensional data. It seems there is a Something-seq paper every day, and this work has created a tremendous amount of data. Sometimes the data is pretty noisy due to low capture rates, batch effects, PCR biases, and more. Moreover, better tools to automate cell-type annotation are needed.

Single-cell sequencing is now building a parts list of individual cells. Whereas we had a parts list for individual humans but they did not fully recapitulate the complexity of biology. Single-cell probably doesn’t create a full picture by itself, but it is a major step forward in understanding biology and disease. For example, the human kidney, interactions between immune cells and antigens, tumor microenvironments, and more have been more accurately profiled because of these tools. With a better mechanistic understanding, we have a better shot at creating better medicines and products for human health.

In short, the main question in single-cell sequencing is - what does 10X or Akoya enable? 10X dominates the R&D part of the market and Akoya dominates clinical applications. Both companies are in an incredible market position and would be hard to usurp. As a result, new companies can think through new applications in oncology, autoimmunity, neurodegeneration, and more to build on top of. New immune cell profiling companies are springing up to find novel mechanisms to pursue in immuno-oncology and autoimmunity. 23andMe could even start integrating single-cell sequencing to their product line. New diagnostics can be created along with more accurate organoid models. Finding new insights from the spatial arrangements within cells is a new frontier. GWAS showed the power of new data helping generate better hypotheses. Single-cell sequencing is some orders of magnitude better in terms of scale and resolution. With this new data, inventors and founders should be able to ask better questions to understand biology and disease.