Axial - Curative

Surveying great inventors and businesses

Axial partners with great founders and inventors. We invest in early-stage life sciences companies often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you - email us at info@axialvc.com

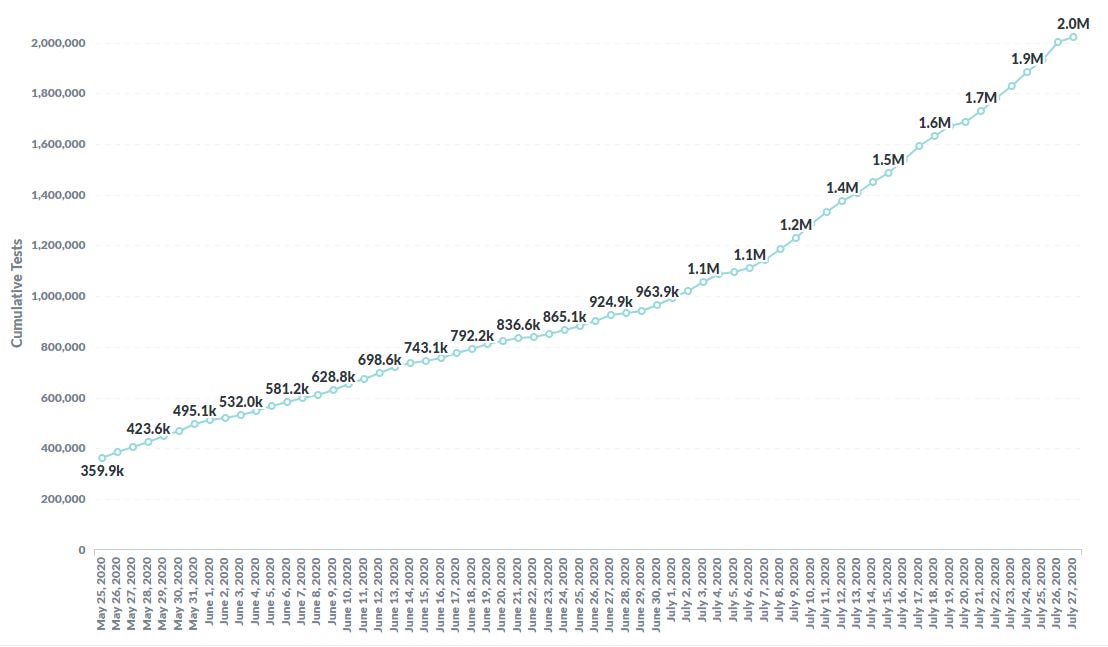

Curative is a unique case study in diagnostics on how to scale from nothing to dominating a market. The company has done over two million COVID-19 tests in under 5 months representing ~8% of all tests done nationwide. Objectively, the company is just getting started given the massive demand for COVID-19 tests. Their rise to prominence is all the more impressive given how 3 founders starting with nothing beat all of the entrenched players (i.e. LabCorp, Abbott) and publicly-lauded COVID-19 testing services (i.e. Chan-Zuckerberg Initiative, IGI), each exponentially better capitalized.

This case study is appropriate now given the lead Curative has gained. It’s like 40-0 and it's halftime - we still have a long way to go to get out of the COVID-19 era. This analysis is broadly applicable to situations where speed is of the essence like a pandemic, war, or a natural disaster. The ability for a company like Curative to succeed is mainly enabled by two things:

Infrastructure and know-how ready-to-go

Belief/boldness that the FDA will approve most things backed by some data and correspondingly, payments will be figured out

For Curative, this helped them move quickly in a new market. These features are also found in COVID-19 vaccines where Vaccitech, Moderna, BioNTech, and Novavax have taken the lead. Also for antibodies with Regeneron and AbCellera as leaders. And Lonza in manufacturing. Curative is a little different than all of these companies because it didn’t exist up until a few months ago. Curative is a successful example where a scrappy founder beats out incumbents in such a short period of time.

Curative was founded by Fred Turner, Isaac Turner, and Vlad Slepnev. They all came from the previous company Fred founded: Shield Bio (originally called TL Biolabs) whose core competency was building infrastructure quickly (like over a weekend). Shield pivoted several times ranging from working on animal health genomics to nanopores. Ultimately, Shield shuttered in January/February of 2020. However, without Shield Bio, Curative would not exist.

Around the time that Shield was being wrapped up, the COVID-19 pandemic was beginning to spread in the US. Surprisingly, not many companies or people were doing much. In Berkeley, I was amazed to still see old ladies in the gym and large groups of people walking around town. Didn’t they know a pandemic was in China and was coming to our shores? Curative got started February/March of 2020 taking all of the good people from Shield and quickly moved into COVID-19 testing. This was a risky gambit. At the time, large incumbents like Quest or Labcorp were assumed to have the capabilities to scale up testing. How was Curative going to compete in a commodified market? There’s no real obvious technical moat - COVID-19 tests often just use RT-PCR. This is where the team’s past experience at Shield proved to be invaluable.

From Shield, they had several contacts in Los Angeles, mainly Jeffrey Klausner, who would get Curative set up with a CLIA lab and up-in-running. This allowed the company to do initial studies to get an emergency use authorization (EUA) from the FDA, which allowed the company to start rolling out their saliva tests nationwide.

There are two parts of Curative’s model that makes it unique versus others:

Focusing on spit-in-a-cup tests (their EUA covered this) where many others are now just catching up here. This was really important to reduce the requirements for swabs as well as minimizing the manpower required to do a given test. This speed is unprecedented, and the FDA would not have moved so quickly if it were not for the pandemic.

Getting governments to pay for tests; first the city of LA then the Air Force with a long list of customers ranging from cities, military branches, and universities

After the EUA, Curative’s success was driven by execution, which they have done a brilliant job at. The company has well over a thousand employees with $100Ms in revenue that likely is ARR if this pandemic lasts several years. Curative is an incredible example of an agile company taking over a billion dollar market in under 6 months.

The story is still yet to unfold, but some of the key lessons Curative’s meteoric rise that might be applicable to other public health companies specifically those that respond to crises are:

In a crisis, get started and figure out the details along the way

This requires having the infrastructure ready-to-go

Governments have to be the payor

The FDA will approve most things if the data is somewhat plausible

Focus on rate limiting steps, which might not always be obvious

Rapid deployment capabilities are essential - a company has to be the marines not the army

Key findings

With a lab set up and a relatively secure supply chain, Curative got to work to secure a EUA so they could commercialize their tests. The team got to work and in about ~2 weeks, they generated the data necessary for the filing - https://www.fda.gov/media/137089/download They used a RT-PCR test to measure the COVID-19 viral loads in patients and discovered that for individuals that had already tested positive and under supervised self-collection, the results from the standard nasopharyngeal test matched perfectly with the oral fluid (i.e. saliva) one. With this result, Curative got their EUA and a massive competitive advantage early on with their ability to conduct saliva tests.

The market for COVID-19 tests globally is in the $100Bs. With cases likely to slow down and reemerge (image below) over the next few years until prophylactic antibodies and vaccines are approved. Maybe this market doesn’t exist ten years from now, but it's a massive opportunity for Curative or any other diagnostic company for that matter to jump into.

The key question is what does Curative do with the free cash flow they generate? Plow it back into the company or distribute it to shareholders? If the former, Curative could be a case study on how to build an enduring business starting with a business model focused on short-lived sales. If the latter, the company is easily worth $1B. We’ll see.

Technology

The key relationship for Curative was with Jeffrey Klausner who had previously consulted for Shield Bio. Klausner was instrumental in identifying and operating the CLIA lab, KorvaLabs, that Curative needed. Curative acquired the lab about 2 months later. The team repurposed KorvaLabs from a sports anti-doping test center to one focused on COVID-19 emphasizing ways to reduce the requirement for certain supplies like swabs as well as securing access to extraction kits. COVID-19 is an RNA virus and isolating RNA is notoriously difficult mainly due to RNA’s 2’ hydroxyl. In every molecular biology lab around the world, a special bench is kept wiped down for RNases and kept clean. A key bottleneck that emerged early on for COVID-19 tests were RNA extraction kits. Curative struck up a deal early on with Norgen Biotek to secure their own supply of kits.

With a lab set up and a relatively secure supply chain, Curative got to work to secure a EUA so they could commercialize their tests. The team got to work and in about ~2 weeks, they generated the data necessary for the filing - https://www.fda.gov/media/137089/download They used a RT-PCR test to measure the COVID-19 viral loads in patients and discovered that for individuals that had already tested positive and under supervised self-collection, the results from the standard nasopharyngeal test matched perfectly with the oral fluid (i.e. saliva) one. With this result, Curative got their EUA and a massive competitive advantage early on with their ability to conduct saliva tests for people that are symptomatic. This reduced the company’s need for swabs and increased the ease-of-testing, which has helped them grow so rapidly. Their preprint can also be found here.

Interestingly, a couple weeks later Rutgers also got an EUA for an at-home COVID-19 saliva test. The group there wasn’t really commercially-minded and didn’t expand to other areas. Curative’s and the group at Rutgers use of media for nucleic acid stabilization, Zymo Research’s DNA/RNA Shield kit for the former and Spectrum Solutions kit for the latter, likely played a role in their positive results for their saliva tests. Remember, COVID-19 is an RNA virus and RNA is extremely unstable in the open environment.

Only now are others trying to catch up. The IGI at Berkeley is doing saliva test studiesnow. Saliva testing is not included in Labcorp’s EUA where LabCorp and Quest are most focused on pooling tests together as a way to scale up. It seems obvious that incumbents will have to shift over to saliva tests sooner-or-later. In the meantime, Curative is expanding their head start. The key advantage here is Curative’s supply chain and operations. They really don’t have a massive technological advantage but their obsession about operations, everything from sample tracking to kits, is progressively building out their moat.

Market

The market for Curative is pretty self-evident even at the time of the company’s founding. Most individuals knew that millions of people needed to be tested for COVID-19. However, most people didn’t think a new company would do a good part of the tests. Conventional wisdom thought incumbents obviously would dominate.

This turned out not to be the case. Part of it was technical and Curative’s focus on spit-in-a-cup tests. The other part is Curative’s ability to get large institutions to pay the company directly:

Los Angeles (at least $50M in revenue; April 2020)

Air Force (at least $50M; April 2020)

Florida ($10Ms; April/May 2020)

Alaska ($10Ms; April/May 2020)

Delaware ($30M; May 2020)

Texas ($45M; May 2020)

George Washington University ($10Ms; May 2020)

DoD (~$30M; July 2020)

Chicago ($10Ms; July 2020)

Texas A&M ($16M; July 2020)

The market for COVID-19 tests globally is in the $100Bs. With cases likely to slow down and reemerge (image below) over the next few years until prophylactic antibodies and vaccines are approved. Maybe this market doesn’t exist ten years from now, but it's a massive opportunity for Curative or any other diagnostic company for that matter to jump into.

Business model

Curative’s business model is still evolving. Overtime, this is where it will get interesting for the company. With the cash flow generated from COVID-19 tests, that will not last forever, what does the company do next?

Right now, Curative completes COVID-19 tests paid for by the state. They charge $150 per test (although prices are/were up to $325 in some instances) where each one costs them around $60-$80. The company has been creative with test delivery using drive thrus and recently introducing kiosks (image below). In short, Curative’s business model is pretty straightforward. As they get more scale, they get further ahead of the competition and more competitive with incumbents as they get their act together. The key question is what does Curative do with the free cash flow they generate? Plow it back into the company or distribute it to shareholders? If the former, Curative could be a case study on how to build an enduring business starting with a business model focused on short-lived sales. If the latter, the company is easily worth $1B. We’ll see.

Publicly, there are some hints on what Curative wants to do next beyond diagnostics. They have a project focused on challenge testing for COVID-19 vaccines. They could also get into epidemiology, and use their patient data to track COVID-19 mutations’ infectivity and mortality rates. I will stop the speculation there though. Let’s see what Curative announces over the coming 6 months.

Ultimately, Curative is a useful and inspiring case study on how to build a billion-dollar business in the matter of months in the face of large incumbents and a pandemic.

Special thanks to Zachary Sun for the help here.