23andMe is a pioneer in consumer drug development. Relying on the Internet for unique distribution of its genetic-testing kits, the company’s sourcing of patient samples is an incredible moat. The company is one of the few healthcare companies to have a direct relationship with patients. Moreover, 23andMe’s direct-to-consumer (DTC) engine generates some amount of cash ($10Ms annually) providing a different pathway to create new medicines. Most drug companies have a binary cash-flow whereas 23andMe has been able to design a business model with steady cash flow and an increasing ability to develop drugs. As a result, the business ought to have cash as a buffer and ideally valuable options that might provide very large amounts ($10Bs) later on.

The over-the-counter (OTC) model for drugs is much older and worth studying to understand how the DTC model 23andMe is pursuing will likely play out. Companies selling aspirin and tylenol don’t rely on IP to maintain pricing power - they create and maintain brands to attract customers. Instead of making large capital investments up front to make drugs then brand them, DTC drug companies like 23andMe create a brand in order to make their drug program potentially more successful. It’s still to be determined if this large amount of data will make drug development generally easier; more likely there will be specific diseases where 23andMe has a major advantage in and can bring transformative medicines to patients. Like many great business models, 23andMe has taken more than a decade to execute on its plan (founded in 2006). Anne Wojcicki (co-founder and CEO) and her team have done a great job ethically running the business and sticking to the long-term plan that is on a path to create new medicines.

Key findings

By bringing the costs of a product down ~10x, 23andMe was able to grow the largest genetic data set so far, and having the core of the company based on scientific integrity has allowed 23andMe to begin to have an impact on user’s health.

The journey of 23andMe’s business model is truly unique enabled by the ability to dominate a category, discipline, and long-duration of capital, so new DTC businesses need to rigorously understand what tools have emerged to make a new use case widely accessible.

23andMe’s DTC model is not being fully rewarded for its value where the market undervalues prevention and only is interested in simple, actionable results that lead to a drug or surgery. As a result, 23andMe’s most valuable path forward is toward drugs - very high margin products - requiring different expertise and new partners.

Technology

The underlying technology powering 23andMe is composed of relatively simple tools. But at the company’s number of users (>5M), the data becomes pretty complex. As 23andMe transitions to whole-genome sequencing, when the cost matches the company’s current kit prices, the potential to match an individual’s genetics to cures becomes more likely.

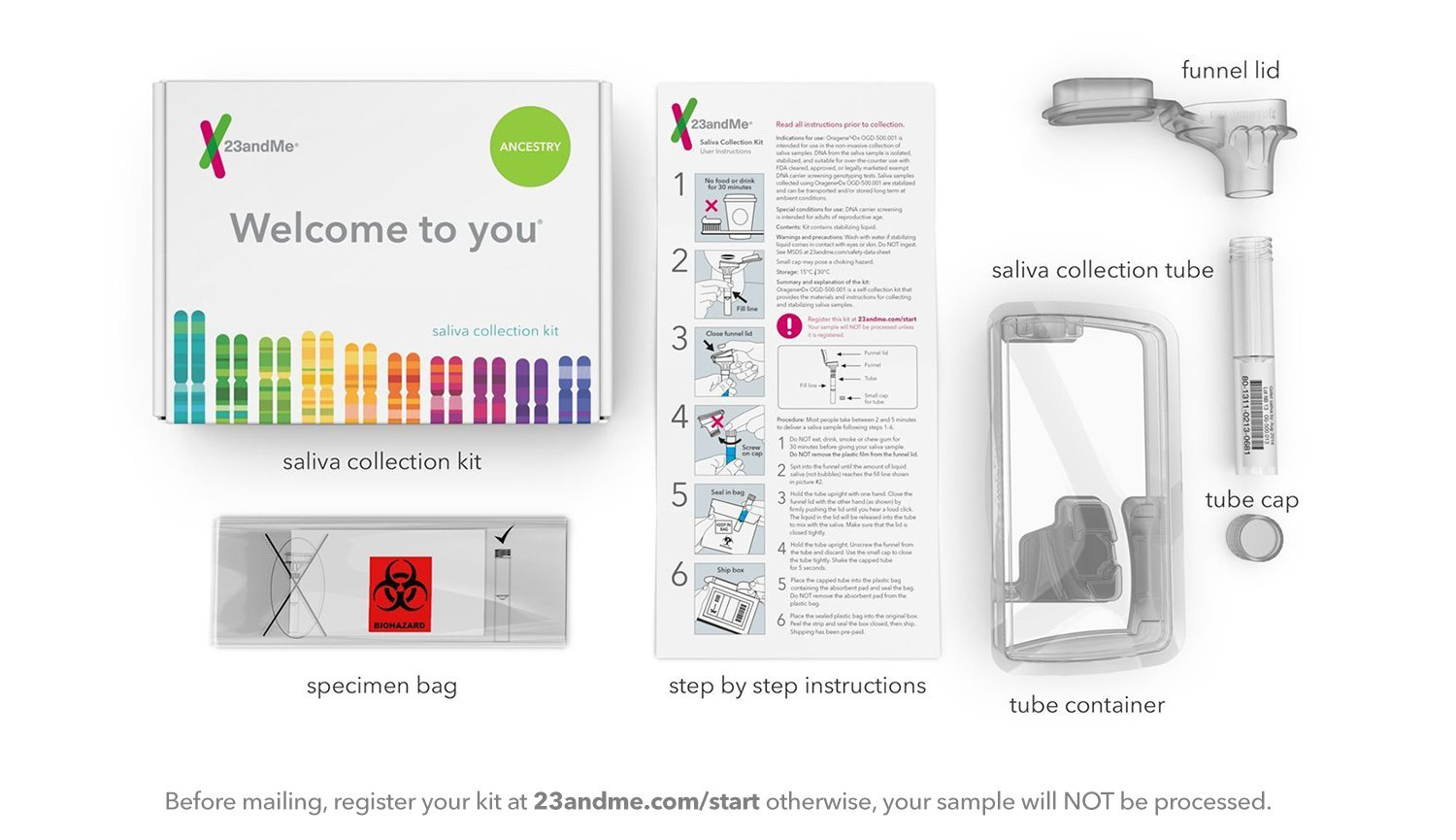

23andMe sends users a saliva collection kit (image below of ancestry kit) in order to analyze their genomes. The kit itself had nothing unique but the company’s insight of where to distribute them was a breakthrough - get exposure in the style section instead of NEJM articles. Early on, 23andMe would host celebrity spit parties to generate buzz around the product; the first day, the company sold ~1000 kits.

Source: 23andMe

23andMe has relied on Illumina chips to measure an individual’s genetic diversity through single-nucleotide polymorphisms (SNP). Over time, the number of SNPs has steadily increased to over 600K to identify genetic markers associated with over 250 diseases now. ISOGG has a great overview of 23andMe’s chip technology and how it’s progressed over time - https://isogg.org/wiki/23andMe#Chip_versionsIn short, a chip has a set of probes that can detect SNPs in an individual. While Illumina is a sequencing provider building out the infrastructure for genomics, very similar to how Nvidia has grown, 23andMe is an increasingly important channel for the company. As 23andMe has grown in popularity so has its ability to have power over its supplier (Illumina) - 23andMe initially used a generic chip but has build able to design a custom chip (Illumina Infinium Global Screening Array) to measure specific SNPs, which becomes a technical moat. Knowing what to measure is just as important as sequencing - this is a major reason why results can have major differences between 23andMe and Ancestry.com; both have very large data sets but each measure slightly different genetic markers.

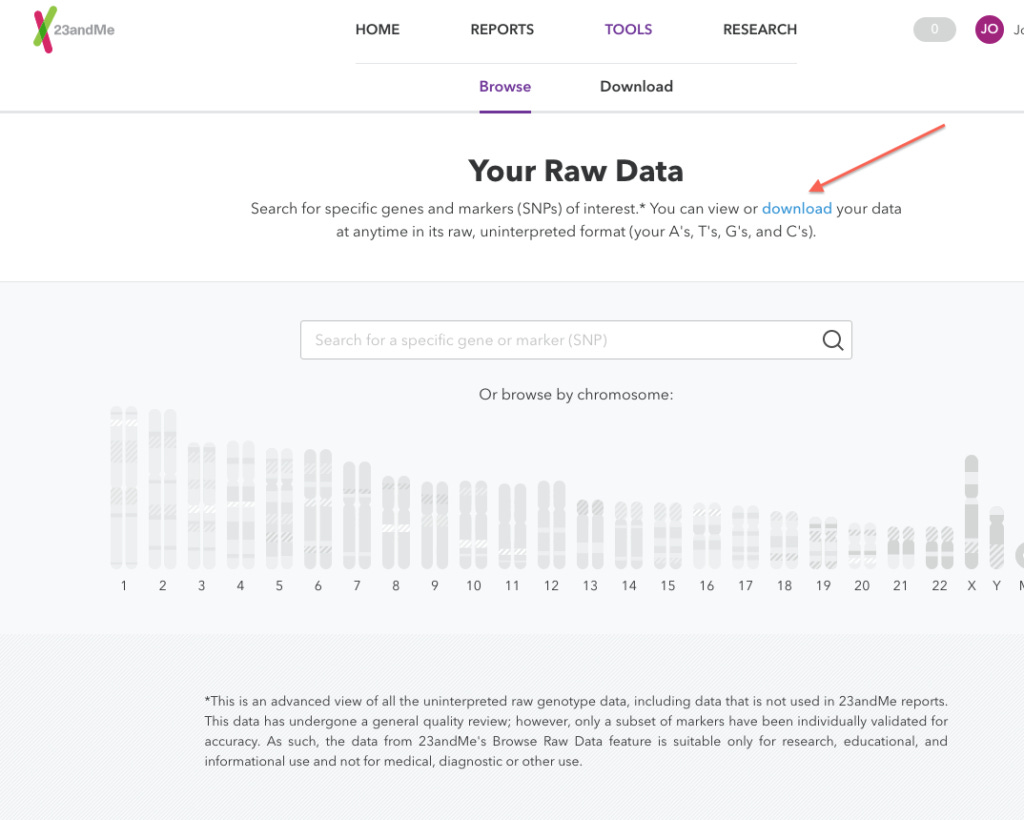

Lastly, 23andMe’s customer-focused mission aligns with portability of data and easy interpretation (image below). Data from 23andMe is probably the only DTC genetics company to allow their data to be analyzed by any tool (Infinomeis interesting to use). Gwernhas a decent overview of his results. Companies like Ancestry.com rely on data lock-in and overtime this advantage becomes less important as sequencing costs come down. Simply humans can be resequenced; as a result, our genetic data is inherently open source (this might not be true for microbiome, liquid biopsy data). To remain compelling, 23andMe offers a suite of tools around the data - over 50 clinical reports based on peer-reviewed studies and over 80 research reports from early scientific results - to make interpretation seamless giving users not only the ability to look into their ancestry but study their own pharmacogenetics, carrier risk, and more:

Source: 23andMe

Ultimately, 23andMe has had technical success by bringing together three relatively straightforward inventions - a kit, chip, and analysis toolkit into a new product. This approach is very similar to what SpaceX has been able to accomplish in the rocket industry - by bringing existing components together in a new way drive costs down 10x; for 23andMe offering a test for ~$100s that would cost a customer possibly thousands of dollars if they did it on their own. This is the core technical breakthrough for 23andMe. By using this unique product, the company created a dataset unparalleled in scale. Around 2013, the company had an important decision to make - continue to grow and meet metrics or cooperate with the FDA. By choosing the latter, 23andMe has been able to bring the first DTC genetic tests to market. In 2013, after receiving a letter from the FDA, 23andMe could have just focused on growth and ignored regulation and it would have seemed normal especially in Silicon Valley. But this wouldn’t have been the right thing to do for the long-term durability of the business, and it took a lot of courage and having the investment partners with long-enough duration of capital to slow down and work with the FDA. Over the last ~6 years, 23andMe has turned this potentially company-destroying event into a major competitive advantage.

Now 23andMe has several FDA-authorized diagnostic tests. With over 5M customers and growing, these tests ought to improve (i.e. versioning life sciences products). Many of these tests have some utility, but right now, it often recommended to do a follow up test; an important example for 23andMe is BRCA. As this path is pursued, 23andMe will likely follow what Color Genomics, another great business to profile, has been able to do: physician-ordered, bundled counseling, next-generation sequencing, and actionable results. It’s exciting that 23andMe is bringing tests to patients in new ways, but it is now entering into a highly competitive diagnostics market where no one company has historically had a monopoly of tests. For 23andMe, it’s very important to know where their data set has a competitive advantage and where it doesn’t. A business like Color might own the oncology genetic diagnostics market; whereas, there are certain classes of genes that 23andMe has much higher, diverse coverage than other companies that are relevant for disease (i.e. Parkinson’s).

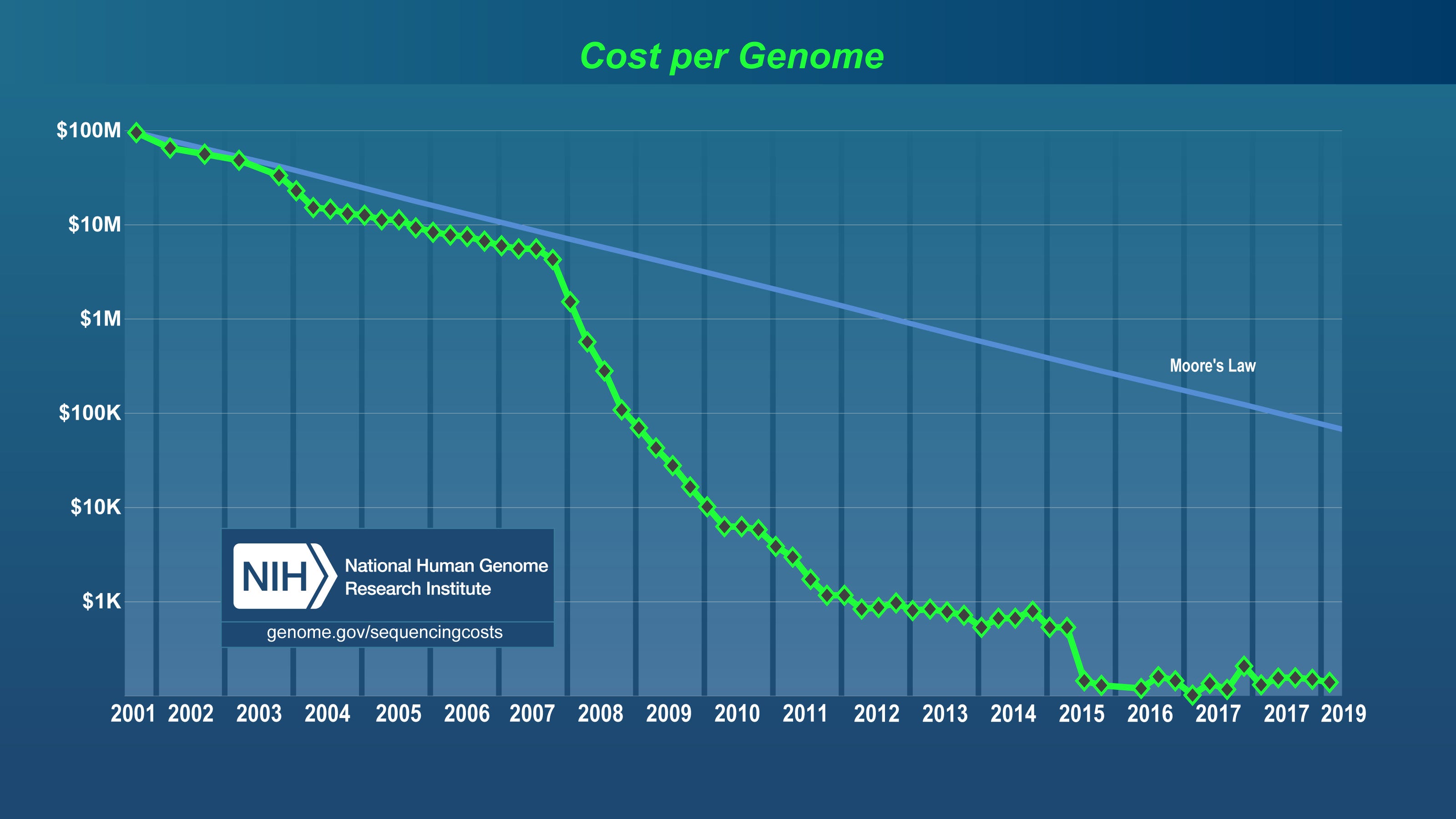

About 2 decades ago, deCODE Genetics was founded to genetically study around 1/2 of the Icelandic population with a similar premise as 23andMe. Although deCODE’s data set is still around, the company did not bring useful tests to market and overestimated the value of genome-wide associations. What changed was super-exponential decreasing costs of sequencing (image below) and Web 2.0 that allowed 23andMe to build the largest genetic data set. To avoid this fate, the company has executed on its same plan (same OKRs over the last 10 years or so) to develop/validate new biomarkers ultimately creating new medicines and management tools (i.e. Virta). For the former, to make a drug, you need a diagnostic first - for example, Parkinson’s still relies on monitoring symptoms; in particular, PD is a massive opportunity for 23andMe. This type of work helps with target discovery. Although, target discovery itself is not that valuable, but the ability to validate them easily is very important - just knowing a gene is associated with a disease is not enough; a lot more work needs to be put in to derisk the target. From here, 23andMe can be part of the drug development process. This pathway relies on tests that become widely used enabling particular data around diseases and genes to improve.

By having the core of the company based on scientific integrity, 23andMe has built trust with its user base to have the opportunity to translate their collective data into new drugs. To accomplish this goal, 23andMe has to take privacy extremely serious (in order to maintain opt-in rates of around 80%) as health/genetic data is probably more valuable than social media data. The product’s value proposition is very high. 23andMe helps gives people more control over their health and work on prevention in a country where prevention is not currently valued due to incentives (i.e. functionally corrupt healthcare system in the US). Similar to how other at-home tests have transformed the world and met pushback from the healthcare system like pregnancy tests, 23andMe's product has pushed the Overton window in the field on what is acceptable. Simply by treating users as a participant not a subject, 23andMe is on the path to pioneer customer-centric drug development.

Source: NIH

Market

The DTC genetics market has been growing since the 1990s. The first set of companies were mainly set up by academics and ended up in a series of bankruptcies/asset sales due to a lack of demand or a useful product. Over time, with growing awareness among consumers and increasing access, the market is still relatively small with total annual revenue in the $100Ms that might get to $1B in the next five years or so. This growth has been driven by lowering costs and better distribution. The DTC market is only attractive as a beachhead or if more diagnostic tests move from the clinical model to the DTC model. The latter is unlikely without a single-payer system or more transparent pricing of tests/drugs. As a result, the market is currently dominated by 23andMe, Color, and a few others for the purpose to themselves move into clinical diagnostics and drug development.

For clinical diagnostics, 23andMe has potential to find niches in a market with billions of dollars of revenue accessible. To generate value here, the company would have to move toward physician-recommended tests. Despite the extreme competitiveness across diseases and settings, making most investments in the field unattractive and maybe acting as a prelude for what is to come in the drug industry as diverse modalities come to market, 23andMe has a shot to reconfigure testing and prevention of disease. Color has made more traction in clinical diagnostics and probably serves as a stronger case study to understand what works.

For 23andMe, the most promising market is drug development. The ability to offer a medicine to users that actually treats and possibly cures the ailment is incredibly valuable. Going straight to drug development gets the company the potential to own a very high-margin product and with 23andMe’s improving data set, possibly tilting the odds in their favor. A recent analysis found that success in the clinic increases to 25.9% from 8.4%when a drug has a coupled biomarker. With well over a third of new drug approvals referencing biomarkers, 23andMe can possibly discover new biomarkers and corresponding drugs for diseases that have genetic drivers. Obvious markets are rare diseases ($10Bs), Parkinson’s ($Bs), and Alzheimer’s ($10Bs). That’s a lot of potential for 23andMe, but figuring out how to accrue value in these markets is going to require partnering with other companies and potentially adding new capabilities to validate targets and find valuable molecules.

Business model

23andMe’s business model created a unique sourcing engine from a lot of hard work and the sequencing and Web 2.0 waves that coincided together. Their DTC genetics model was more-or-less a very long fishing expedition that is now returning to harbor. The ~10 year journey required discipline and long-duration capital (helpful to subsidize growth bringing prices from $999 to $99-$199). This was enabled by the possibility of 23andMe dominating their market by bringing together genomics and Web 2.0. So similar DTC health models just coming out need to convey the ability to dominate their category (i.e. rigorously answering ‘What’s changed?’).

As 23andMe aggregated users and their genotypes, the business model shifted into improving their health (image below). The stakes are much higher now, but with the track record of the team and their ethics, the company has the potential to make better and more predictable medicines. In this market, this is probably the only way this business model can accrue significant value. This is mainly because prevention is not really rewarded right now. As a result, 23andMe will be part of the push toward fee-for-value and benefit from it, but will have to be the owners of new medicines:

Source: Revenue & Profits

The DTC-centered drug business 23andMe is pursuing has quite a few similarities to how the OTC drug market developed. Merck pioneered selling drugs to consumers in the 1800s focusing on alkaloids. When the pharmacy industry was just emerging, the chemicals and drugs were essentially coming from the same companies. Germany was an epicenter of the industry due its high concentration of chemistry inventors, Switzerland benefited as well for not honoring patents at the time, and the US where companies like Pfizer emerged creating anti-septics for the Civil War. Once antibiotics were discovered and used, the blockbuster model for drug development began forming. Many of the world’s most important drug companies originally started selling drugs directly to people. But as the actual causes of diseases were discovered, these companies pointed their chemical synthesis capabilities to make drugs. Companies like Pfizer and Eli Lilly created a new industry. The OTC drug market now is worth over $100B but hard to get a large piece of - selling drugs for things like allergies that don’t require a prescription doesn’t give companies a lot of pricing power. The OTC market has some revenue potential but it’s not as compelling as a blockbuster drug - successful drug companies went where they can accrue a lot of value. Similarly, the DTC market is interesting but making medicines is much more lucrative. Whereas the original drug companies built chemistry engines and transitioned from an OTC model to drug development, 23andMe is beginning to use its genetic discovery engine to create new therapies for a unique targets. To build a great drug company, 23andMe needs access to new modalities from small molecules to antisense RNA. The company has some internal projects but has focused on partnerships.

23andMe is working with Genentech finding unique variants in Parkinson’s. GlaxoSmithKline (GSK) made a $300M equity investment to form a partnership to pursue a target for Parkinson’s as well. GSK will provide the chemical matter and 23andMe will help with patient enrollment and provide new targets. Similarly, Calico partnered with Ancestry.com to study the genetics of longevity. Ultimately, the use of these data sets for drug development is exciting. However, for 23andMe and similar business models, the economics of each deal is really important. Target discovery is not enough to garner good enough terms to build a large business in drug development - validation, improved predictivity, molecule libraries are necessary components. The long-term potential of 23andMe is in their ability to aggregate patient data and own the medicine. There’s a chance for 23andMe to make drugs whose price doesn’t solely depend on IP but brand and the related services. This fits into the overall theme of transitioning toward a full-stack, outcomes driven model. On this point, Roche is slowly moving toward this themselves bringing together their drug pipeline with Foundation and a few other platforms. Just as the last 10 years for 23andMe was exciting and winding, the next 10 years look just as long and exciting as the business model transitions toward drug development.